What will happen in the insurance market in 2024?

What will happen in the insurance market in 2024? | Insurance Business America

Insurance News

What will happen in the insurance market in 2024?

Experts offer their predictions

Insurance News

By

Emily Douglas

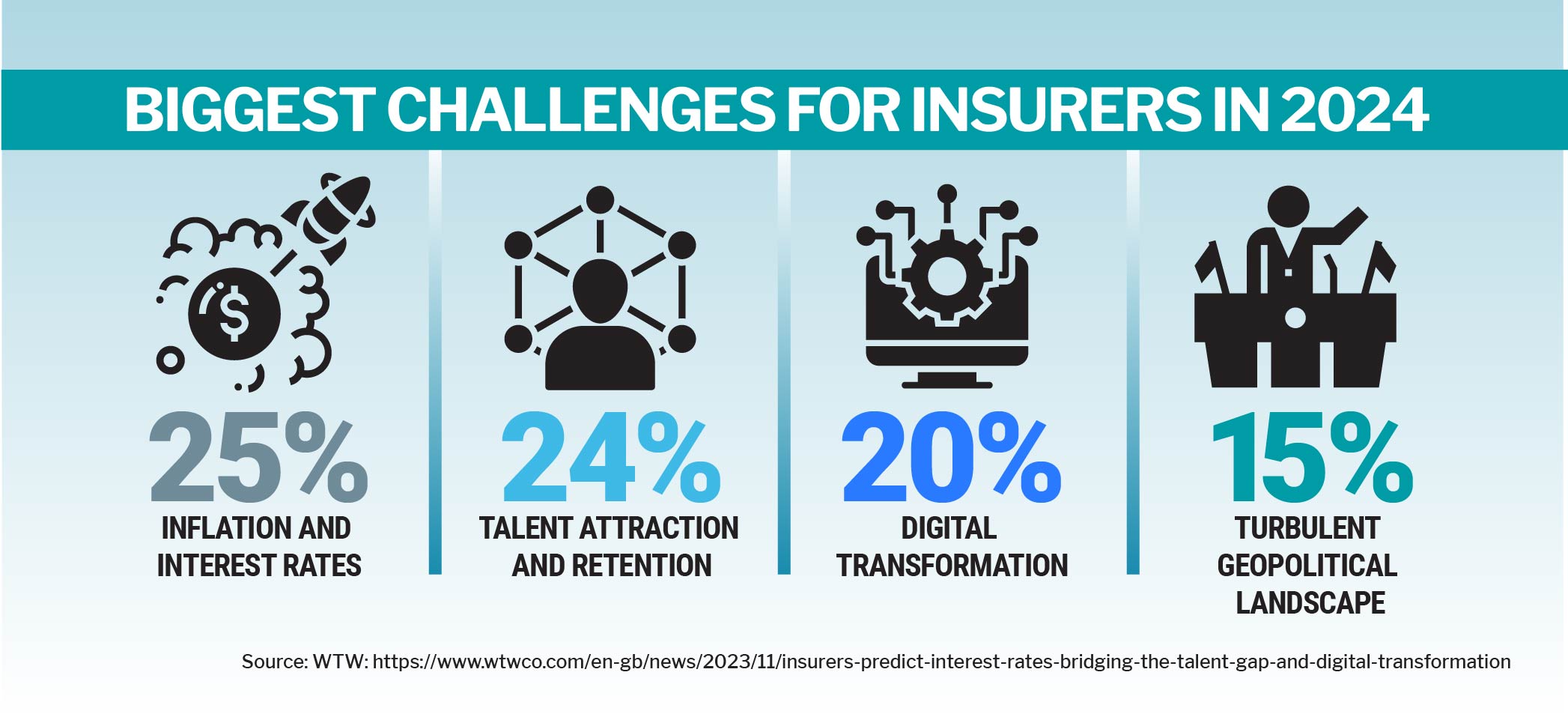

As we arrive in 2024, the insurance landscape looks set to evolve again. From inflationary concerns, to a talent pipeline crisis, to the rising importance of cyber, insurers can expect to have a lot on their plates in the coming months.

A recent report from Deloitte shed light on a few concerns – including the rise of commercial property premiums by 20.4%, climbing expenses impacting personal lines insurers and even a hit on motor repair costs in the auto carrier space.

But is it all doom and gloom? Or are there certain changes insurers can look forward to in the new year? In that vein, Insurance Business asked a collection of the sector’s biggest names and leaders to shed light on their predictions for the market in 2024 and beyond.

Brace for disruption: Kyle Matthews , director of sales and distribution, Hartford Fire Insurance Company

“I envision the future as being disrupted by technology – and with that there being opportunity to think about how we, as people, relate to each other and do business in this new wave. Leveraging technology with automation and AI is going to be a real opportunity to rethink and reimagine how the support team interacts with the underwriting team. As you see in Amazon and Apple starting to get into the auto space and taking on their own capacity – in some respects trying out insurance products and PE involvement – venture capitalism is being injected as is some other capital in the industry.

“I’m optimistic about the opportunities we have to change the industry for the better and use what’s been done to build on it – to help change the narrative around insurance being a dorky thing, to the career destination of choice.”

Retention, retention, retention: Laura Zoltan, senior vice president, strategy & distribution, Arch Insurance Group Inc

“I’m now focused on attracting and retaining talent. Previously my focus was on results, but as I’ve grown as a manager and leader, I realize it all begins with talent. It’s the people that ultimately drive Arch’s culture and make it a unique and special place to work.

“The question is not only how we get people to come into this industry, but also how we get them to stay. So a big part of what I’m thinking about in the future is leading from a place of actually understanding what each individual wants out of his or her career. It’s important to realize that not everyone has the same goals and motivations. Not everyone wants to climb the corporate ladder. So I need to take responsibility to ask these questions, and then tailor my approach and style of management accordingly.

“It’s about individual development – something which can easily (and unfortunately) be put on the bac burner. But I think when managers focus on this, it makes employees feel seen, respected and valued, which ultimately drives them to stay.”

Gaining momentum responsibly: Krishna Lynch, assistant vice president, casualty risk engineering, Zurich Resilience Solutions

“The risk landscape is continually evolving, and we have to adjust and adapt. We must have the right mix of partners, stakeholders, and workforce to do that. But we also have to lean into elevating talent and ensuring that we have diverse teams. I think we’re gaining momentum but there’s still a lot of work to do. I think it just requires a little more intentionality.

“With advancing technologies, we have to make sure that we’re integrating new tools responsibly. As we begin to integrate these technologies and use automation to help us solve problems, we have to do so responsibly.

“And I think employee wellbeing and mental health will continue to be huge issues that organizations will need to build sustainability around.”

Mind the cyber gap: Michelle Chia, head of professional liability & cyber, Zurich North America

“The challenge right now that many SMEs and mid-market size organizations face is that they have a cybersecurity gap. They have a difficult time addressing those cybersecurity gaps because they have a lack of access to resources that their larger, more complex, more sophisticated organizations have access to.

“Earlier this year we launched a new cyber insurance policy to address that white space, those gaps. This insurance policy is called the Zurich Cyber Insurance Policy – Concierge Suite. Resilience and risk transfer solutions that go hand in hand. And so, this isn’t just an insurance policy, it’s not just some document that responds when something bad happens. The offering includes access to risk engineering tools and resources through Zurich’s relationships to help organizations close those gaps to improve their cyber resilience.

“Zurich Resilience Solutions has digital capabilities that assist organizations to understand what is happening within their environment – almost like an early detection. Complex and sophisticated organizations often have those detection tools centralized in-house because there are many different areas where they need to detect and protect. Data show that middle market organizations have this need too. The service happens in something like a security room where you have multiple screens to see what’s happening on every floor, but from a cybersecurity perspective – which is pretty cool.”

Tough conversations: Jenna Kirkpatrick Howard, senior vice president, Lockton Companies

“My crystal ball isn’t very clear most days – but I will say there’s no signs that the property insurance market is improving quickly. We may not see the large spikes and increases that we’ve seen for the last 22 consecutive quarters but we will continue in a challenging market with limited capacity coming in. We are also starting to see lability insurance lines harden.

“I think 2024 is going to be a year of some tough conversations and good planning in advance. Alternative risk products like captives, fronting and structure solutions will become of more interest as my clients start to think about how to take on more risk so they’re not beholden to the hard cycles of the insurance market.”

Capitalizing on expansion: Berri M. Willis, associate vice president – managing director, Burns & Wilcox

“The hard market has been an opportunity as well as a challenge. I think finding the opportunity in that challenge is where you’re going to be successful, not focusing on what you don’t have but what you do have and then capitalizing on it. In the Carolinas, we’re a very CAT exposed area and we’ve capitalized on our strengths with Lloyd’s of London and our aggregate capabilities.

“We’re looking to continue to grow expansively in 2024 – particularly when I look at talent recruitment and goals for 2024 with offices throughout both North Carolina and South Carolina. We’re looking to expand Burns & Wilcox as a whole to great lengths. I want to be at the forefront of that, bringing on talent recruitment, more experts in the field, focusing on many different lines of business, different niches, and different departments. And I think it’s just a recipe for success.”

Related Stories

Keep up with the latest news and events

Join our mailing list, it’s free!