Reinsurers were capital challenged even before hurricane Ian, Aon data shows

Even before hurricane Ian slammed into Florida, a cohort of reinsurance companies tracked by broker Aon were capital challenged this year, as financial market volatility and macroeconomics dented capital for the group.

Aon publishes data on the financial performance of a group of leading reinsurance carriers, known as Aon’s Reinsurance Aggregate.

These reinsurance firms underwrite more than 50% of the world’s life and non-life reinsurance premium and are therefore a reasonable proxy for the sector as a whole.

The 21 reinsurance firms tracked are: Alleghany, Arch, Aspen, AXIS, Beazley, Everest Re, Fairfax, Hannover Re, Hiscox, Lancashire, Mapfre, Markel, Munich Re, PartnerRe, QBE, Qatar Insurance, RenRe, SCOR, Swiss Re, SiriusPoint and W.R. Berkley.

Explaining the volatile backdrop and macro-economic situation, Aon said, “The first six months of 2022 were notable for an unusual amount of volatility in the capital markets. The pandemic-related inflationary spike that began in 2021 was exacerbated by Russia’s invasion of Ukraine in February, prompting aggressive interest rate hikes that, in turn, have raised fears of recession. For US stock markets, it was the worst start to a year in more than half a century.

“The long-awaited adjustment to higher interest rates will ultimately boost reinsurers’ profitability via higher investment returns, but the speed of the change is having a significant short-term impact on asset values. In addition, high inflation is creating uncertainty around future and legacy loss costs, which may need to be addressed through higher pricing and/or additions to prior year reserves.”

Despite all of this, the reinsurance firms reported robust premium growth and generally strong underwriting results, Aon said, but their, “overall earnings and equity positions were heavily impacted by unrealised losses on investment portfolios, driven by rising interest rates, widening credit spreads and declining stock markets,” the broker explained.

The effects of this are widely felt across insurance and reinsurance, but particularly evident in industry capital levels.

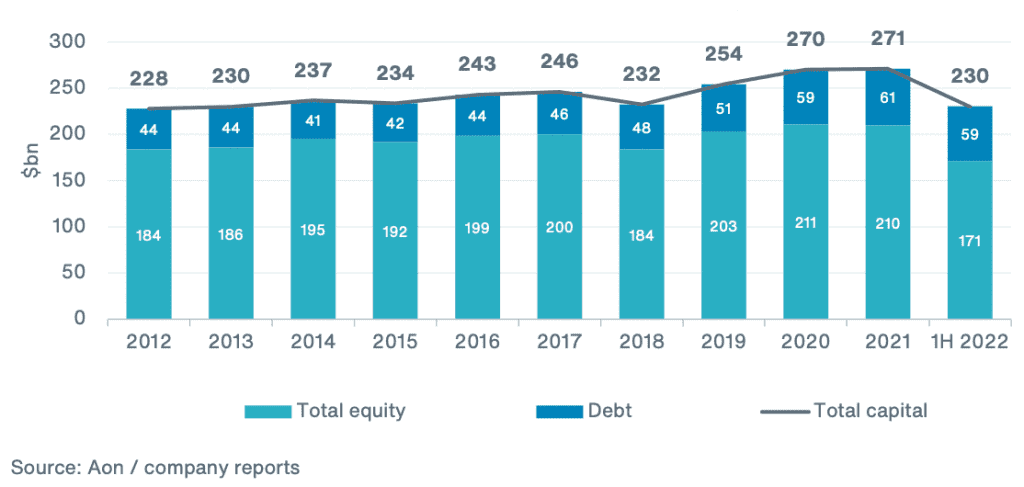

The impacts are perhaps most obvious when you look at the capitalisation of these reinsurance firms and how that declined through the first-half of 2022.

Aon explained that, “Total capital reported by the 21 ARA companies fell by 15% to $230bn over the six months to June 30, 2022, partly reflecting strengthening of the US dollar relative to the euro. Total equity fell by 18% to $171bn, driven by significant unrealised losses on investments, while debt was broadly stable. As a result, the debt-to-total-capital ratio rose to 25.7%, from 22.5% at the end of 2021.”

Unrealised losses have been the main driver for the decline in equity capital among these reinsurance companies, responsible for just over $30 billion of the drop.

Aon explained, “The value of low-yielding bonds already held on balance sheets is being written down because they are less attractive on the secondary market in a higher interest rate environment. However, these assets are generally held to maturity and the value usually recovers as that date approaches (known as the ‘pull-to-par’ effect). The unrealised losses are therefore expected to unwind over time.”

While these unrealised losses may unwind and valuations recover of the assets held, the immediate impact of a reduction in equity capital will have ramifications for some reinsurance companies and for the market itself.

It means a further reduction in available reinsurance capital, which comes at a time when many of the levers these reinsurers could have used to help them expand capital, such as efficiently priced retrocession or use of third-party capital partnerships, may be more challenging to source or raise.

Mike Van Slooten, Head of Business Intelligence for Reinsurance Solutions, commented, “The long-awaited adjustment to higher interest rates will ultimately boost reinsurers’ profitability through higher investment returns, but the speed of the change is having a significant short-term impact on asset values.”

Van Slooten also noted the influence on inflation and what this may mean at upcoming reinsurance renewals, “In addition, high inflation is creating uncertainty around future and legacy loss costs, which may need to be addressed through higher pricing and/or additions to prior year reserves.”

With interest rates continuing to rise, reinsurers could face more pain that affects their capital.

Aon said that, on top of losses from hurricane Ian, “In addition, interest rates are continuing to rise, which will further pressure total investment returns and reported book values.

“Overall, 2022 seems destined to be another poor year for reinsurer earnings.”

A further decline in sector capital can’t be ruled out before the end of the year renewals, especially as hurricane Ian’s losses will have broad ramifications for these reinsurance companies.

This market environment could have been an opportune time for retrocession strategies, particularly those that are structured to help reinsurers make the most of their equity and rated capital levels, when it comes to their capacity deployment.

Those kinds of retro solutions are few and far between nowadays and with retro even more dented after hurricane Ian, with a lot of collateralised retrocession set to be trapped, there could be an opportunity for those with retro capacity available to deploy to step in and assist any capital challenged reinsurers around the end of the year.