What is a Loan Clause When Buying a Home in Ireland?

What is a loan clause when buying a home in Ireland?

If you’re on the lookout for a new home, you should be familiar with the key clauses that make up a typical contract for sale.

You’ve probably also read about the importance of getting these right before you sign on the dotted line.

However, while many clauses are simple enough to understand, there are a few that are less straightforward — particularly those related to the purchase itself.

If you’re unclear on what each clause means, how can you know if they’re right for your situation?

Legal jargon is notoriously difficult to decipher, so you will need to get a solicitor involved to ensure the consumer protection laws you need are present in your contract.

Especially the Subject to Loan/Mortgage Clause

Why is a Loan Clause important?

If you’re buying a home in Ireland and you don’t have the luxury of the Bank of Mummy and Daddy, then you’ll need to schlep up to the nearest lending institution and beg for a mortgage.

The bank will promise to loan you a big load of dosh to buy a dream home bijou style, boutique, character-filled one bed in Ballybejock.

However, this loan offer usually lasts for a maximum of 6 months before you have to apply all over again.

So, what happens if you sign contracts for a new build and your loan offer expires before you get to draw down your mortgage?

Simple, you re-apply.

But this time, the bank refuses to play ball as you got a pay cut, or had a child, or stuck a tenner on the Grand National or farted at Mass or whatever crazy rules the banks have these days for pulling their approval.

You’re kind of screwed as you have paid a 10% non-refundable deposit, and you can’t complete the purchase.

Even worse, in sneakier contracts, the seller may be able to come after you for any losses they incur!

This is why, my home buying reader, you need a Loan Clause / Subject to Loan Clause to protect yourself.

And it’s not just me saying this. The learned Law Society of Ireland has warned that purchasing without a Loan Clause is unsafe.

Legally unsafe means you’d be bananas to even think about it.

Do all sale contracts in Ireland have a loan clause?

Generally, yes, it’s a standard clause to protect the home purchaser, but some developers will only add the Loan Clause if requested to do so.

They argue that they can’t get finance for the next development of houses unless they have unconditional contracts for the ones already sold.

Unfortunately, it’s a seller’s market, and people are desperate enough to sign anything if it means they’ll be able to move out of their parent’s back room.

Should you pull out of the sale if your contract doesn’t have a loan clause?

Tough question, it depends on how confident you are that you’ll be able to complete, and this comes down to your health (see below) and job security more than anything else.

But if the Law Society is warning people off, I would heed their advice.

Can you get a Loan Clause added to your contract?

Yes, this is where your solicitor earns their corn.

What to look out for in the absence of a Loan Clause?

The three main reasons the lender won’t re-approve your loan are

1) Satisfactory valuation

Valuations shouldn’t be an issue these days, with house values in Ireland on the rise.

2) Change in your financial situation

This can be for a multitude of reasons.

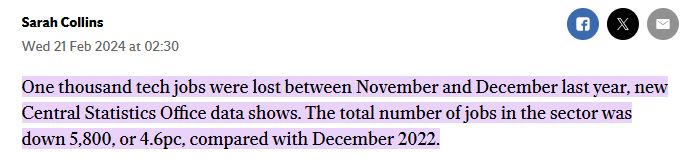

Job cuts especially in the tech industry at the moment.

Pay cut.

Stupidly taking out a new car loan since you were loan offered – you wouldn’t do that, would you??

2) Inability to get mortgage protection

To draw down a mortgage in Ireland, you need a mortgage protection policy to clear your debt if you die before paying off the mortgage.

Them’s the rules.

In the vast majority of cases, people get mortgage protection without any issues.

However, if you have an underlying health issue, you may struggle to get cover.

And, unfortunately, you may only realise your health could be a problem waaaaay after signing the contract.

If you can’t get mortgage protection and signed a contract without a Loan Clause, you will lose your deposit.

Can you arrange Mortgage Protection in advance?

If you intend to sign a contract that doesn’t contain a subject to Loan Clause, you need to have your mortgage protection in place in advance.

Now, I don’t mean just have it arranged, accepted, and ready to go.

You should issue and start paying for your policy well before you need it.

So, let’s say your new build completion date is in 12 months. You should activate your policy today.

Why?

Because if you suffer any health issues in the next 12 months, the insurance company can review and revoke their acceptance.

The only way to prevent this from happening is to activate your policy. Once the insurer issues your policy, it is set in stone and cannot be taken from you.

How do you arrange Mortgage Protection if you have a health issue?

We’d love to help. It’s what we specialise in, so we know what we’re doing.

If mortgage protection is possible, we’ll get it for you at the lowest rate and in the least amount of hassle.

Here’s another blog you may find useful:

How to Get Life Cover if you have an Underlying Condition

Over to you

Be sure to read through your entire sales contract, and take time to understand any difficult clauses before you sign on the dotted line. If there’s something you don’t understand about a clause, never be afraid to ask for clarification from your solicitor.

And if there is no Loan Clause, request one. If the seller refuses, then tread carefully.

If you’d like help arranging your mortgage protection, please complete this questionnaire, and I’ll be right back.

Alternatively, if you’d like a chat with me first, you can schedule a callback here.

Thanks for reading

Nick

Editor’s Note | We published this blog in 2021 and have updated it since.