Switching Life Insurance Companies: How and When to Change

Johnnnnny!!!

Yes Mary

I heard a fella on the radio saying you could get life insurance for €10 a month. How much are we paying?

Dunno Mary; I’ll check with Nick; remember that funny lad from Offaly that we liked??

Ah, Johnny, he was a bit of a dose, have you nobody else?

—-

Howaya Nick, Johnny here; how much are we paying for life insurance?

Lemme check….eh, €117 per month, Johnny.

But Mary can get it off the radio for a tenner.

Does the radio know you’re both smokers, that Mary has diabetes, and that your Dad had a heart attack at 40?

Eh, probably not. I’ll ring you back – thanks.

Mary, he can’t do any better.

I told ya he was a dose.

🤨

How to Switch Life Insurance Providers

Paying for insurance is a P.I.T.A.

Car insurance, house insurance, gadget insurance, pet insurance, life insurance, health insurance, the list is endless.

It’s all a massive waste of money until you make a claim, and then it’s the most important few quid you could ever spend.

I looked at my life cover recently to see if I could save a few bob, so I thought it would help outline the thoughts going through my head.

How Can You Get a Better Deal Of Your Life Insurance?

Your first step is to get a quote to check if what you’re currently paying is good value compared to what’s available in the market.

Punch in your details (date of birth, smoker status, type of cover, amount of cover, years remaining on the policy and hey presto, out pops your new quote)

You can get an instant quote on our website.

You should consider switching if the quote you see is less than what you currently pay.

If the quote you see is higher than what you pay for your cover, then at least your current cover is good value.

Are You Comparing Like with Like?

Be careful here; it can all go wrong if you switch cover purely on price.

Your second step is to ensure the cover you’re quoting for is the same or better than your current cover.

Here are some simple questions to ask about the replacement policy.

Is there a conversion option?

Is it dual-life cover?

Is the replacement policy’s serious illness definitions easier or more difficult to claim?

Is the serious illness cover accelerated or additional?

WARNING!

Some older serious illness policies paid out for ALL types of cancer.

The newer policies payout according to the severity of the cancer.

Be very careful if you have a policy that will pay out for any cancer diagnosis.

Do not replace this policy.

Any New Health Issues Since You Took Out Your Policy?

As we age, the pounds get harder to shift, leading to higher blood pressure, increased BMI and raised cholesterol.

So it’s no wonder life insurance is generally cheaper when you’re younger and slimmer.

Unfortunately, the ageing process makes it harder to “switch and save”.

If you have suffered any serious health issues like cancer (unless in remission over seven years), heart attack or stroke, I can confidently say you’re better off staying where you are.

The loading/increase on a new policy will make your current premium look more competitive than an oil-funded soccer team.

Are You a Social smoker (even the odd cheeky one?)

If you smoked like a train when you took out your policy, and now your body is a temple, fair play, you should get a lower premium.

However, even if you’ve had a social one in the last 12 months or you vape, and your GP knows about it, then you, my friend, are a smoker.

If you’ve started to smoke since you took out your current policy – fuggedaboudit, you’re not going to get cheaper life insurance.

Fun fact: even if you vape 0% nicotine e-cigs, you are a smoker for life insurance purposes.

The Application Itself – All Those Health Questions?

So, you still want to switch?

Your current provider must have really turned over you.

Some shyster sold you that one!

The next step is to complete a new life insurance application form to switch to a new insurer.

Depending on your age, this may trigger the need for one or more of the following:

Health Questionnaire

Nurse screening

Report from your GP

Medical exam with your GP

Independent Medical Exam

4 and 5 are rare – really only for those with whopper health issues or who need whopper amounts of cover.

1, 2 and 3 are pretty common if you’re 50+

I’m saying you might have to be poked and prodded a bit to switch insurers.

Can You Reduce Your Coverage to Get a Lower Premium?

Have you checked if your current insurer will let you reduce your cover without going through underwriting?

If your current policy has a conversion option, you can convert it to a new policy—maybe you don’t need as much coverage as you did (kids are grown up, the mortgage is smaller, etc.), but you’d like a longer-term policy.

But if your insurer has told you “no dice,” and you’re happy with all the steps above and still want to switch, well, then we should talk.

Can You Transfer Life Insurance to Another Provider?

It’s unlike car, house, or even health insurance, where you can switch the same coverage to a new insurer.

With life insurance and mortgage protection, you have to start again with a new application.

Can You Get Money Back if You Cancel Your Life Insurance?

Before they cancel, people always ask if they can cash in their life insurance policy.

Unfortunately, the answer is a big fat no.

You see, the insurer keeps your premiums as payment for the protection they offered while they had you covered.

If you had claimed, they would have paid out a big ol’ chunk of change, and for that promise to pay, they pocket your premiums.

But a cashback life insurance policy Royal London offers may pique your interest.

What Happens if You Switch Life Insurance Companies?

Pretty simple answer – your old insurer no longer has to pay out if you die or get sick.

Your new insurer takes on this risk, and you pay them a few quid every month.

Can You Have Two Different Life Insurance Policies?

Yes, you can have multiple policies – I looked at this in detail in a previous article:

Can you have multiple life policies?

Do You Have Enough Life Insurance?

I can’t stress this enough – life insurance exists solely to replace your income when you die.

Because if you’re dead, you can no longer earn a living (unless poltergeists are in demand).

But your family will still need an income to cope financially.

Let’s say you earn €50,000 and intend to work for 20 more years.

That’s potential earnings of a cool million.

If you go and do something stupid like dying, your family lose that income.

Life insurance leaves a lump sum of money to replace that income so your family can maintain a decent standard of living.

Compare your current life insurance amount with your potential earnings until retirement.

If there’s a big shortfall, you should review your life insurance.

Do You Have The Right Type of Life Insurance?

There are four types of life insurance.

Mortgage protection

Don’t be fooled into thinking this is for your protection.

It’s for the bank.

You die; the policy clears your debt.

Did you know the bank gets the payout on a serious illness claim on your mortgage protection policy?

Mortgage protection doesn’t protect your family.

If you want to safeguard your family’s financial future, you need life insurance too, which leads on nicely to:

Life Insurance

I call it family protection because it will leave a lump sum of money to your family when you die.

They will use this to replace your monthly paycheque.

If you have a mortgage and a family, you should have two separate policies: one to cover your debt to the bank and one to protect your family.

Don’t try to combine mortgage and family protection.

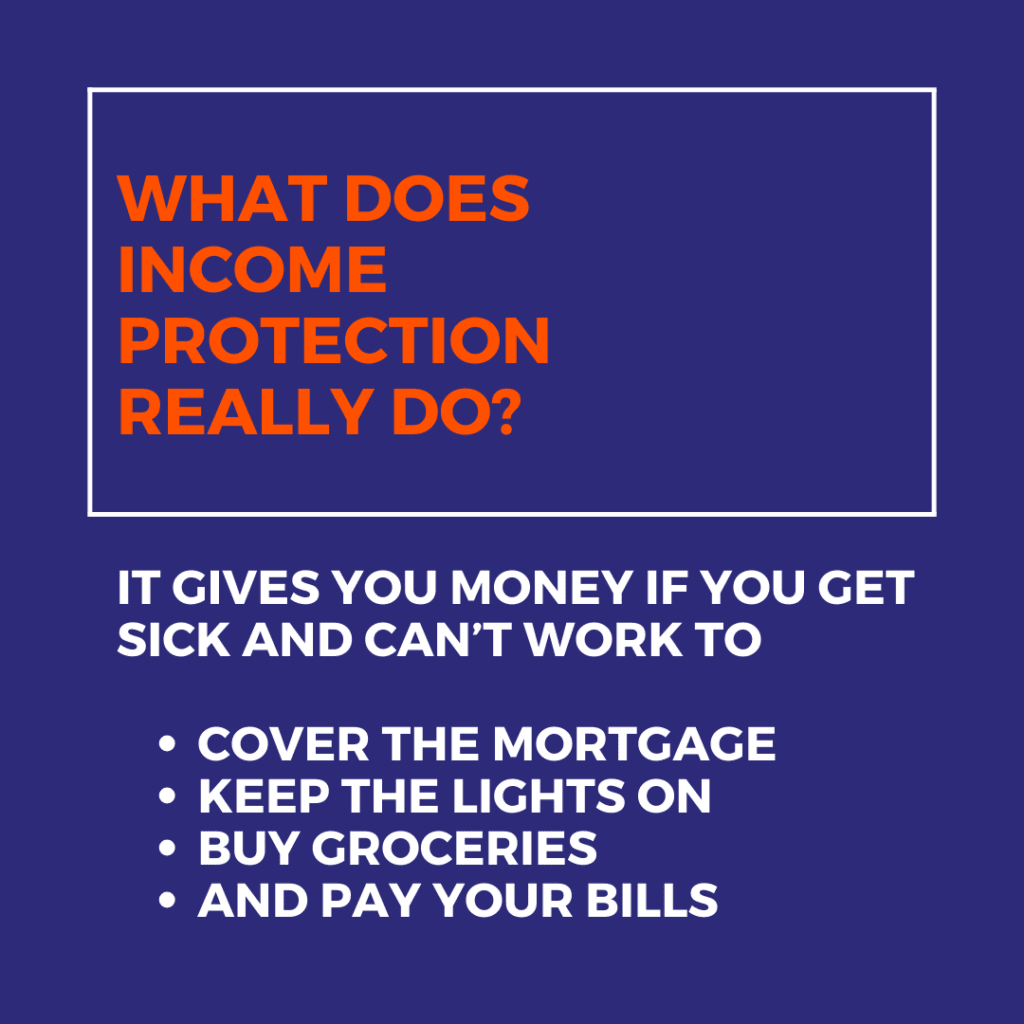

Income Protection

This is the most important type of insurance you can buy.

Actually, it’s the most important anything you can buy.

How long would your savings survive if you couldn’t work long-term?

What if I told you €50,000 in savings would last just 17 months (drawing down €3000 per month).

What if I also told you the average duration of an income protection claim is seven years (84 months)?

How long would your savings last if you had to replace your income long-term?

Serious Illness Cover

We only recommend illness coverage if you can’t get income protection.

What’s the Difference Between Income Protection & Serious Illness Cover?

Do You Have the Correct Term on Your Life Insurance

A lot of people still buy long-term 35-year policies.

I think this is crazy.

If you put a shorter-term life insurance policy in place, you can buy more coverage for the same price.

For example, a €500,000 policy over ten years would cost the same as a €300,000 policy over 30 years.

You should buy a cover until your youngest child reaches 25. If your youngest is 2, you need a 23-year term life insurance policy.

But always add a conversion option.

This lets you extend your policy as many times as you like without answering any health questions, guaranteeing you can get cover in the future even if your health suffers.

What about Buying Life Insurance that Reduces?

This is a clever way of buying more coverage when the kids are young for a lower premium than level-term life insurance.

Read this blog to learn how it works

How To Arrange Life Insurance (for less)

Over to you

It’s possible to save money on life insurance, but if your policy is over five years old, you’ll struggle unless you were ripped off in the past.

Life insurers are smart.

Every year that passes means you’re less likely to save money, so you’re more likely to stick with them.

And there’s nothing more profitable than life insurance policies that stay on the books long-term.

Instead of focusing on saving money, you should check if your current cover is fit for purpose.

Or, more importantly, do you have income protection?

I cannot stress enough how important that particular type of policy is.

Please complete this questionnaire if you’d like me to look at your current cover.

![]()

![]()

See you on the other side.

Thanks for reading

Nick

Editor’s note: We published this blog in 2020 and have regularly updated it.