Stocks Pare Gains on Market Jitters, Bonds Fall

U.S. stocks rose as traders wagered the worst of the banking turmoil has passed, though gains pared sharply in early afternoon trading after headlines that a Russian aircraft collided with a U.S. drone. Treasuries fell.

The S&P 500 advance was cut in half as geopolitical concerns and comments from ratings companies on the financial sector underscored the fragile sentiment on markets jolted by the biggest American bank failures since the financial crisis.

Equities rallied earlier after investors speculated government support for the banking system would prevent broader contagion.

First Republic Bank triggered a volatility halt as it peeled back its relief-rally gains after S&P placed the company on watch negative. The stock was still up more than 20%. The Moody’s Investors Service cuts its outlook on the sector on the heels of the trio of banking collapses over the past few days.

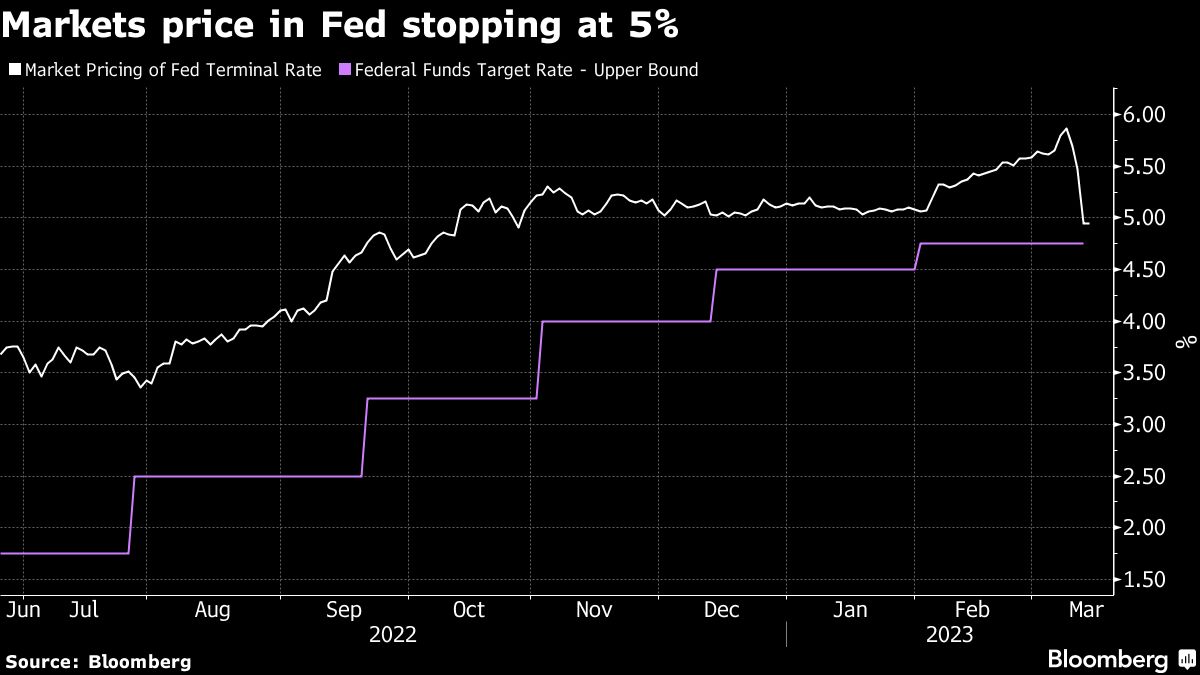

The two-year Treasury yield climbed to 4.3% — following a three-day swoon that was the biggest in decades amid the tumult — after data showed inflation remained elevated in February.

Swaps traders now expect the Fed to lift rates by a quarter percentage point. Odds of an increase had slipped to nearly 50-50 on Monday. The dollar was little changed versus major peers.

Recent Data

U.S. consumer prices rose 0.4% in February, meeting economists’ forecast. The closely watched core CPI number — which excludes food and energy — increased 0.5%, just ahead of the median estimate of 0.4%.

Anxiety on an expanding bank contagion was more subdued on Tuesday as the Cboe Volatility Index or the VIX, fell 15%, the most in eight-months. The fear-gauge had topped 30 for the first time this year on Monday.

Treasuries have been whipsawed in recent days — with a measure of volatility climbing to the highest since 2009 — and banking shares plunged as the collapse of Silicon Valley Bank and two other U.S. lenders prompted wagers the Federal Reserve will pause its hiking cycle and even cut interest rates to stabilize the financial system.

Tom Essaye, a former Merrill Lynch trader who founded “The Sevens Report” newsletter, expects that the data will keep the Fed on track to raise rates 25 basis points next week.

“Given the bank troubles, this report isn’t bad enough to put 50 bps back on the table, but if the Fed wants to maintain credibility on inflation, then this report says they have to hike again next week and not signal they are done,” Essaye wrote.

Goldman Sachs Group Inc. economists as well as asset managers from the world’s largest actively managed bond fund, Pacific Investment Management Co., said the Fed could take a breather on the policy rate following the collapse of SVB. Nomura Holdings Inc. economists took it one step further, saying the Fed could cut its target rate next week.

“Overall, this is an inflation update that, taken as a sole input, would suggest that a 25 bp hike next week is a foregone conclusion,” said Ian Lyngen, rates strategist at BMO Capital Markets. “Alas, the regional banking stress leaves next week’s decision as a wild card until there is greater clarity on the success of limiting the contagion to the rest of the banking sector from SVB/Signature.”

Elsewhere in markets, oil extended declines. Bitcoin topped $26,000 for the first time since June. Gold slid after rising in the three previous sessions as traders turned to haven assets.

Here’s what else Wall Street is saying:

“Although the number was higher in core MoM than expected, it is probably not sufficiently so to corner the Fed into hawkishness at the next meeting. Therefore risk assets are able to breathe a sigh of relief here, as the Fed probably has the option to go easy at the next meeting, if they feel the banking system requires it.” — Peter Chatwell, head of global macro strategies trading at Mizuho International

“The CPI number is no game changer. After the events last week, a 50bps appeared unlikely going into the data print today and the slightly stronger than expected core inflation print puts speculation of a Fed pause to a rest.