S&P 500 Hit by Fed-Pivot Rethink on Rate Cuts

Wall Street traders sent stocks and bonds sliding after another hot inflation report signaled the Federal Reserve will be in no rush to cut rates this year. Oil climbed as geopolitical jitters resurfaced.

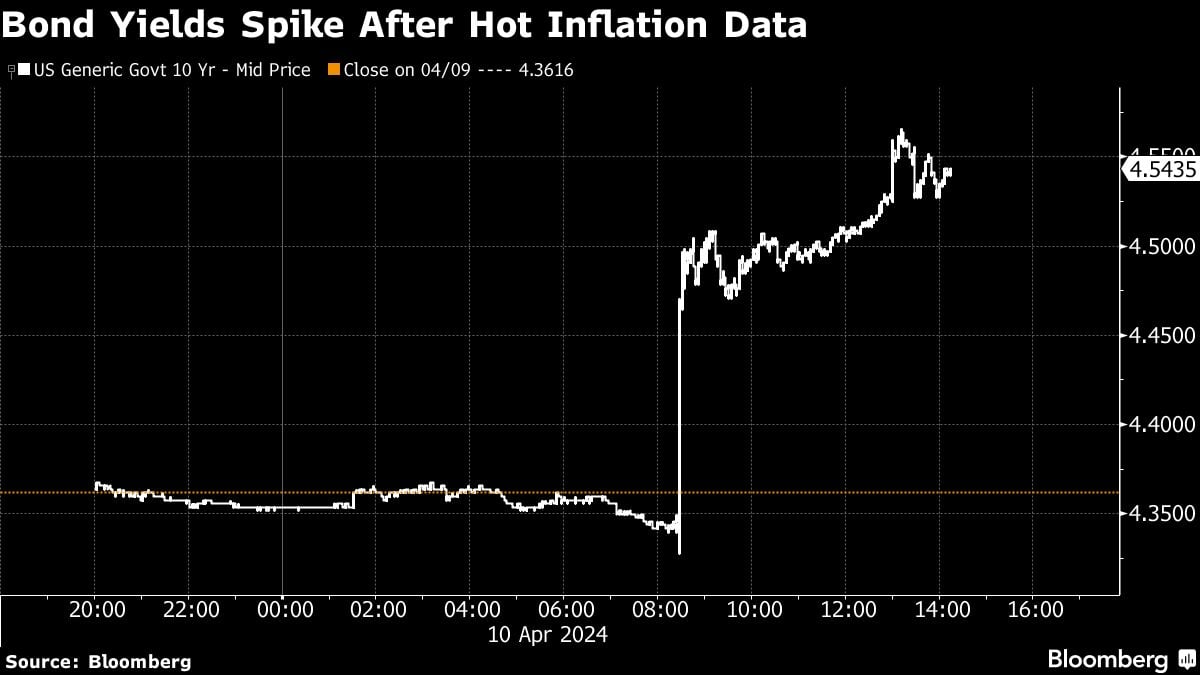

Equities extended their April losses, with the S&P 500 down about 1% as the consumer price index topped economists’ forecasts for a third month. Treasury 10-year yields topped 4.5%. Fed swaps are now showing bets on only two rate cuts for the whole year.

A sharp reversal in oil also weighed on sentiment, with Bloomberg News reporting the U.S. and its allies believe major missile or drone strikes by Iran or its proxies on Israel are imminent.

As the Fed rides the so-called last mile toward its 2% inflation goal, investors’ concern is that the recent price pressures may not be just a “blip” — with the higher-for-longer rate narrative taking hold.

Minutes of the latest Fed meeting showed “almost all” officials judged it would be appropriate to pivot “at some point” this year. But inflation since then has upended market bets.

“It’s often said that the Fed takes the escalator up and the elevator down when setting rates,” said Richard Flynn at Charles Schwab. “But for the path downwards in this cycle, it looks like they will opt for the stairs.”

The Fed minutes also showed policymakers “generally favored” slowing the pace at which they’re shrinking the central bank’s asset portfolio by roughly half.

The S&P 500 dropped to around 5,150. Treasury two-year yields, which are more sensitive to imminent Fed moves, surged 22 basis points to 4.96%. The dollar headed toward its biggest advance since January. Brent crude topped $90 a barrel again.

The March core consumer price index, which excludes food and energy costs, increased 0.4% from February, according to government data out Wednesday. From a year ago, it advanced 3.8%, holding steady from the prior month.

These figures — alongside the jobs report released last week — complicate the timing of the Fed’s rate cuts, according to Tiffany Wilding at Pacific Investment Management Co.

Not only there’s now a strong case to push out the timing of the first cut past mid-year, it also strengthens the odds that the U.S. will ease policy at a more gradual rate than its developed-market counterparts, she noted.

“Inflation right now is like the ‘stubborn child’ that refuses to heed the parent’s call to leave the playground,” said Jason Pride at Glenmede. “Two cuts is now likely the base case for 2024. As a result, investors should be prepared for a higher-for-longer monetary regime.”

That doesn’t mean rates are going higher — but the distance to a rate cut is another quarter, according to Jamie Cox at Harris Financial Group.

“You can kiss a June interest-rate cut goodbye,” said Greg McBride at Bankrate. “There is no improvement here, we’re moving in the wrong direction.”

To Neil Dutta at Renaissance Macro Research, Fed officials are still cutting this year, but they won’t be starting in June.

“I think July is probable, which means two cuts remain a reasonable baseline,” Dutta said. “If the Fed does not get a cut off in July, however, investors will need to worry about path dependency. As an example, would September be too close to the election? If not June, then July. If not July, then December.”

Growth vs. Inflation

At the start of the year, the amount of easing priced in for 2024 exceeded 150 basis points. That expectation was based on the view that the US economy would slow in response to the Fed’s 11 rate hikes over the past two years. Rather, growth data has broadly exceeded expectations.

“Easy financial conditions continue to provide a significant tailwind to growth and inflation. As a result, the Fed is not done fighting inflation and rates will stay higher for longer,” said Torsten Slok at Apollo Global Management. “We are sticking to our view that the Fed will not cut rates in 2024.”