Maximize your corporate account return potential with segregated funds

Provide a tax efficient income stream for your surviving spouse

Like many Canadian business owners, you may be holding money in your corporate account in GICs and other short-term investments to avoid market downside risk. Consider segregated funds as an option in your corporate account to maximize investment returns and get efficient tax and estate planning.

An Empire Life segregated fund may be a better corporate account investment than GICs or other short-term investments as it provides;

An opportunity to participate in equity market growth

Protection of capital

A tax efficient distribution to your surviving spouse.

Better investment returns and creating a tax efficient income stream for your surviving spouse can both be achieved by holding Empire Life segregated funds in your corporate account.

Strategy for creating an income stream for your surviving spouse with your corporate account’s money

Many Canadians operate their businesses as corporations including farming, manufacturing, incorporated professionals and other forms of active businesses. The cash flow generated by the business often accumulates in the operating corporation or in a holding corporation and is invested in corporately held assets. If you are the sole shareholder of a corporation or if you and your spouse are shareholders of a corporation with corporately owned assets, you may want to find tax efficient ways to use these assets as part of your estate planning.

Corporate account estate planning objectives

![]() An important part of estate planning is ensuring that corporately owned assets could be used by your surviving spouse to pay for living expenses after you pass away. While GICs and other short-term types of investments provide guarantees and easy access to cash, the low rates of return may prove problematic as Canadians are living longer than previous generations and therefore have longer investment horizons. Empire Life segregated funds provide an investment alternative with the opportunity for growth, while providing protection of capital and enabling a tax efficient distribution to your surviving spouse.

An important part of estate planning is ensuring that corporately owned assets could be used by your surviving spouse to pay for living expenses after you pass away. While GICs and other short-term types of investments provide guarantees and easy access to cash, the low rates of return may prove problematic as Canadians are living longer than previous generations and therefore have longer investment horizons. Empire Life segregated funds provide an investment alternative with the opportunity for growth, while providing protection of capital and enabling a tax efficient distribution to your surviving spouse.

Setting up a segregated fund strategy in your corporate account

To benefit from the higher investment potential and guarantees of a segregated fund;

![]()

Use your corporation’s cash, GICs or other short-term investments to make a deposit in a segregated fund contract. Name the annuitant under the segregated fund contract as yourself and designate the corporation as beneficiary.

![]()

In addition, add a mention to your will to ensure that your holding corporation’s shares are transferred to your surviving spouse when you pass on. This allows for the transfer to be done on a tax-deferred basis thereby not triggering any tax liability upon your death.

![]()

After you pass on, your surviving spouse will own the shares of the holding corporation, which will have received the death benefits in cash from the segregated fund contract.

Illustration of corporate account shareholding structure using segregated funds

Executing the segregated fund strategy using distributions from your corporate account

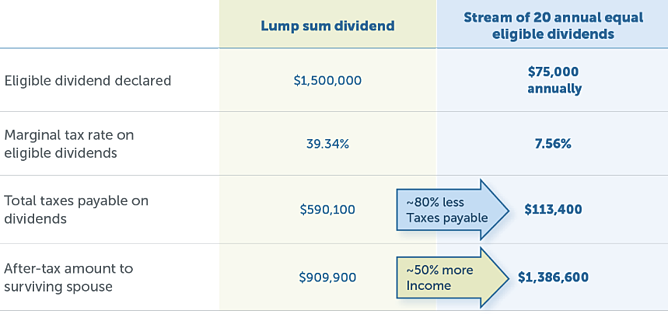

After you pass on, the holding corporation invests the cash received from the segregated fund’s death benefit in a financial product that permits a distribution of regular dividends to your spouse. Your spouse could consider purchasing another Empire Life segregated fund as scheduled withdrawals are available under Empire Life’s Systematic Withdrawal Plan. Distributing the funds as regular dividends over a 20-year period, rather than as one lump sum dividend, makes the cash distributions much more tax efficient.

Example of a distribution of $1,500,000

(Lump sum dividend vs 20 annual equal dividends)

Tax rates applicable in Ontario in 2021.

Tax rates applicable in Ontario in 2021.

The benefits of using a segregated fund strategy in your corporate account

By using a segregated funds strategy in your corporate account you’re able to meet the objectives of:

• An opportunity to participate in equity market growth

• Protection of capital

• Provide a tax efficient distribution for your surviving spouse.

The cash that was initially invested in financial products with lower rates of return is moved into segregated funds, which provide a potential for higher growth. Your initial capital investment is protected because of the guarantees offered by segregated funds and the cash distributions to your spouse will be done tax efficiently after you pass on.

Better investment returns and creating a tax efficient income stream for your surviving spouse can be achieved by holding Empire Life segregated funds in your corporate account.

Speak with your advisor to find out how an Empire Life segregated fund can help you maximize your corporate account investments and achieve your estate planning goal of tax efficient distributions for your surviving spouse.

This document includes forward-looking information that is based on the opinions and views of Empire Life as of the date stated and is subject to change without notice. The information contained herein is for general purposes only and is not intended to be comprehensive investment advice. We strongly recommend that investors seek professional advice prior to making any investment decisions. Empire Life and its affiliates assume no responsibility for any reliance on or misuse of the information contained herein.

Empire Life Investments Inc. is the Portfolio Manager of the Empire Life segregated funds. Empire Life Investments Inc. is a wholly-owned subsidiary of The Empire Life Insurance Company. Segregated Fund contracts are issued by The Empire Life Insurance Company (“Empire Life”). A description of the key features of the individual variable insurance contract is contained in the Information Folder for the product being considered. Any amount that is allocated to a segregated fund is invested at the risk of the contract owner and may increase or decrease in value. Past performance is no guarantee of future performance. All returns are calculated after taking expenses, management and administration fees into account.

® Registered trademark of The Empire Life Insurance Company. Policies are issued by The Empire Life Insurance Company.