Lying About Taxable Equivalent Rate of Return on Cash Value Life Insurance

Podcast: Play in new window | Download

Life insurance agents often talk about internal rate of return (IRR) when discussing cash value life insurance. The term may appear exotic but put in simpler terms, it’s the rate of return you are achieving on the premiums that you pay into the policy. Equipped with this information, we can compare how putting money into whole life or universal life insurance works out against a slew of other options you have available to you.

Personally, I’ve always found the internal rate of return discussion silly. Some clients–mostly those who work in finance–ask about it. And since insurance software can calculate it, it does make life easier versus calculating it yourself. But for most people, the rate of return, in general, is an esoteric notion.

Few people can tell me what having a certain rate of return really means to them. There are plenty of people, however, who believe that simply having a higher rate of return is always the better bet. There are a number of circumstances where I’d agree. But the pursuit of wealth accumulation, retirement planning, and other financial planning-related subjects can be more nuanced than just “give me the highest rate of return you can.”

That being said, insurance agents–who want to sell life insurance–know that people often rank the rate of return highly in terms of importance. So any massaging agents can do to…”enhance?” rate of return (i.e. internal rate of return) is a sure-fire way to convince more people they should buy more life insurance. Right?

Taxable Equivalent Rate of Return

Cash value life insurance (e.g. whole life and universal life insurance) enjoys numerous tax benefits. Chief among these benefits is accumulating and distributing entirely income tax-free cash value (when done specifically/correctly).

Given the tax-free nature of life insurance cash value, many agents argue that simply comparing the cash value accumulation of life insurance to the accumulated value of many other savings/investment options tells an incomplete story. We can’t compare any option that does not avoid tax liability like life insurance–and there are very few options that do avoid taxes like life insurance–because we’ll overstate the benefit received from the taxable options and/or understate the benefits received from life insurance.

So, in order to adjust for this complexity, several life insurers began including the internal rates for return calculations that included an adjustment for the income tax liability. The agent simply plugs in the prospective buyer’s tax rate, and now we know how much extra rate of return he/she needs in other accounts to achieve the same cash value result projected from the life insurance policy. Easy, and certainly not susceptible to any manipulation that might way overstate the needed rate of return to match a life insurance policy–sarcasm light on and glowing red hot.

What is Your Tax Rate?

I’ve been selling life insurance for well over a decade now, and in that time I’ve seen a lot of proposals presented by different agents. Within these proposals, I’ve seen many internal rate of return reports that include this taxable equivalent adjustment. What’s interesting about all of them, is the tax rate they assume. A lot of them are north of 50%.

Now, I’m not here to claim that taxes are too low and need to rise–I just begrudgingly cut two big checks today myself. But assuming a 50% effective tax rate? Should we not question that just a bit?

Average Effective Tax Rate Americans Pay

Most of us are at least somewhat familiar with the U.S. Tax Code with respect to income and its progressive nature. As your income rises, you could eventually go beyond a threshold that subjects you to a higher tax rate on a certain amount of your income.

If, for example, you happen to have income that puts you in the 37% tax bracket–which happens to be the highest bracket currently–that means some of your money is subject to a tax rate of 37%. It DOES NOT, however, means that ALL of your money is subject to 37%. So being in the 37% tax bracket doesn’t mean that you pay 37% in taxes. In fact, very few Americans pay anything close to 37% of their income in taxes.

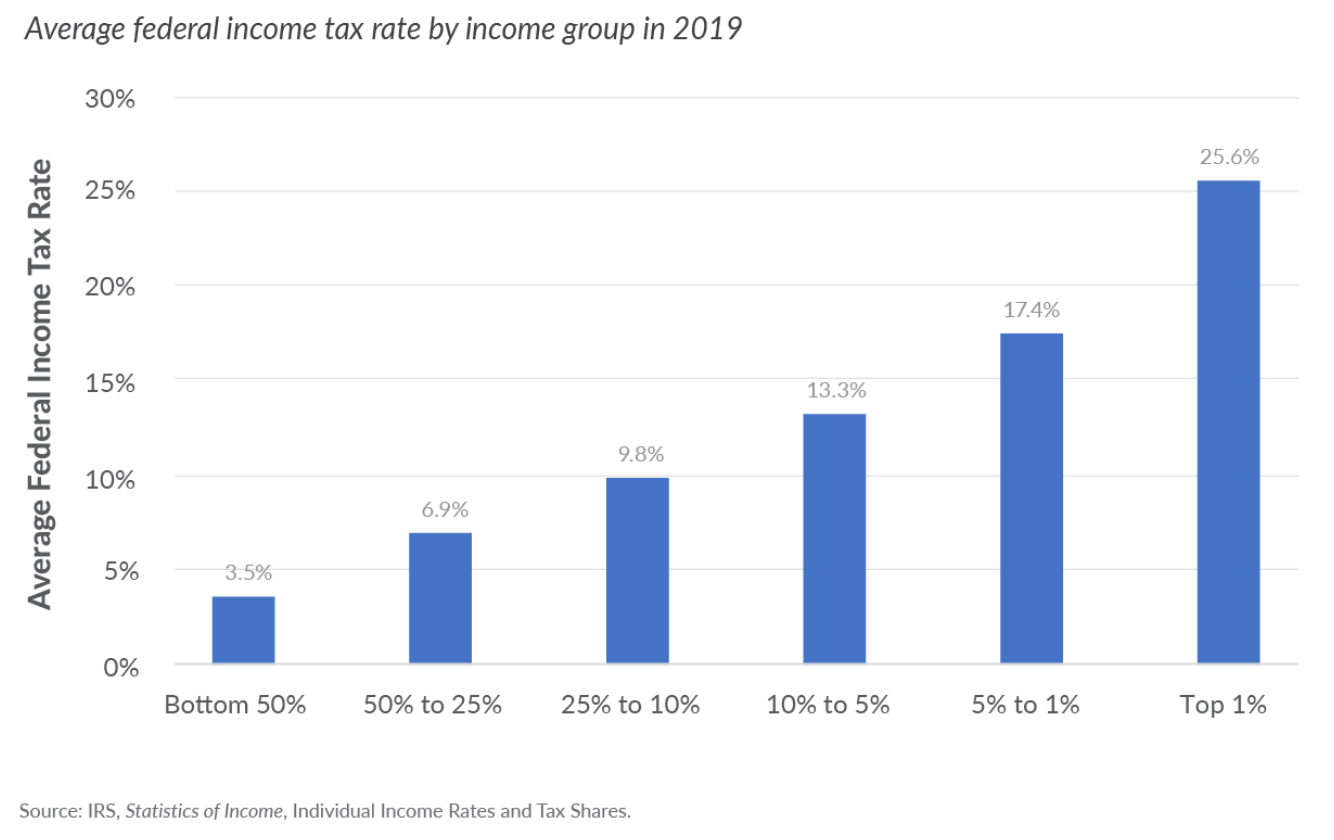

According to IRS data compiled by TaxFoundation.org, the top 1% of income tax filers in the U.S. paid an average effective income tax rate of just 25.6% in 2019–it’s actually gone down slightly since then, but this was the most complete compilation of data, so that’s why I’m citing it.

Notice that none of the other cohorts have an effective tax rate above 20%. It’s worth noting that this data does not include State Income Taxes or FICA. Adding those in will certainly increase the effective tax rates paid, but we’re still a long way from 50%.

Notice that none of the other cohorts have an effective tax rate above 20%. It’s worth noting that this data does not include State Income Taxes or FICA. Adding those in will certainly increase the effective tax rates paid, but we’re still a long way from 50%.

Unreasonable Assumptions Make Us Look Foolish

Many people lie with statistics–there was a great book written on the subject several years ago. But using wildly inflated tax assumptions to make life insurance rate of return look better does more harm to us as an industry than it does to help make more sales.

Few people know what their effective tax rate is, I’m not doubting that. But I think most can reasonably pick out that they do not give up 50% of their income to taxes. They may hate paying them–most everyone does. That doesn’t mean they’ll willingly accept the idea that half their income goes to taxes.

As professionals–some of us fiduciaries with fancy certifications–we have to approach modeling savings and investment options with care in order to help guide our clients to the right decision. Carelessness reflects badly on our industry.