Income Protection for Engineers Working in Ireland

Hello there! 👋

Are you an engineer who wants to protect your income in case you get sick or have a slip, trip or fall that puts you on your back and out of work?

Then you need income protection!

Whether you call it disability insurance, income replacement, or salary protection, it all boils down to one thing – ensuring that you have financial support when you need it most.

I know, it’s not the sexiest topic, but then again, neither is a life without a steady paycheque.

In this article, I’ll explain what income protection is, why it’s important for engineers (and everyone else), and how to choose the right policy for your needs.

I’ll also answer some of the burning questions you have about disability insurance but were too afraid to ask, like

Can I still collect benefits if I’m in a coma but my cat is doing my work for me?

So whether you’re a mechanical engineer, a chemical engineer, a software engineer, a civil engineer, an electrical engineer, a biomedical engineer or just an engineer of your own destiny, grab a cup of tea (or crack open a beer, you might need it), and let’s get started.

Don’t worry, I’ll keep it light and entertaining – no calculus required.

What is Income Protection for Engineers?

Rightio, let’s break this down in plain English.

Income protection, also known as disability insurance or salary protection, is like having a financial safety net to catch you if you fall, providing support and peace of mind when you need it most.

Here’s how it works: if you’re unable to do your job due to an illness or injury, income protection will provide you with replacement money to help cover your expenses.

Think rent or mortgage payments, utility bills, the weekly shop and the other less mundane stuff that keeps you alive and kicking.

But not all income protection policies are created equal.

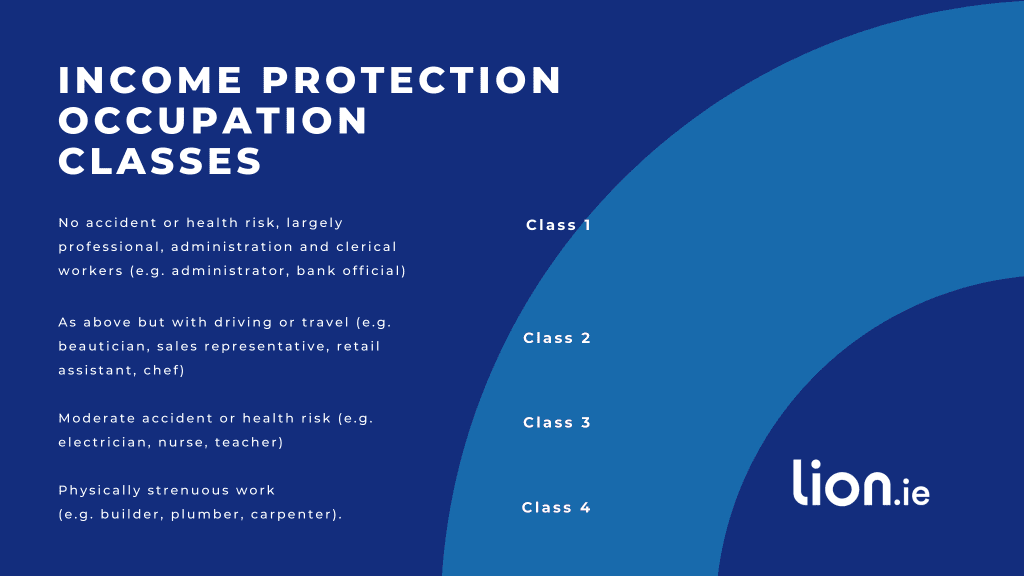

As an engineer, your occupation is likely to be classified as low to medium risk, which is great news for your wallet. But, it’s important to check with each insurer to see how they classify your job because the exact classification can vary from insurer to insurer.

If you’re in a low-risk occupation, like a software engineer, you will qualify for Class 1 lower premiums.

On the other hand, if you are an electrical engineer, be careful which insurer to apply to. The lowest occupation class available is Class 2, however, some insurers will dump you into a Class 4 category so your premiums will be off the charts!

Waiting or deferred periods can range from a few weeks to several months, depending on the insurer.

And the all-important payout?

Well, all the insurers will insure up to 75% of your income (less state illness benefits if you are an employee). If you are a sole trader or director of a limited company paying Class S PRSI, you can insure the full 75%.

And finally, there is the premium you must pay for this protection. We think income protection is priceless but I’m sure you’re interested in how much it’s gonna cost.

The premiums you pay for income protection depend on factors such as your age, health, occupation, and level of coverage.

Here’s a quote for a 33-year-old Software Engineer earning €80,000.

She will get sick pay from her employer for the 26 weeks that she is unable to work.

If she cannot do her job for more than 26 weeks, her income protection will kick in and pay her €48,560 annually until she gets back to work or turns 65.

She will pay the figure in the left column and can claim tax relief annually (see here).

The net cost to her is the smaller figure in the right-hand column.

Why Engineers Need Income Protection Insurance

As an engineer, your job is all about problem-solving and innovation.

But what happens when an unexpected problem arises that prevents you from doing your job?

That’s where disability insurance comes in.

Here are a few reasons why engineers should consider disability insurance:

Your income is essential to your financial well-being.

As an engineer, your income is likely one of your most valuable assets. It’s what allows you to pay your bills, support your family, and save for the future. Without that income, you could quickly find yourself in financial trouble.

Your job may involve physical or mental demands that can lead to injury or illness.

Depending on your area of engineering, your job may involve physical labour, exposure to hazardous materials, or long hours spent sitting at a desk. These demands can take a toll on your health and increase the risk of injury or illness.

You may not have adequate sick leave or other benefits through your employer.

While some employers offer sick leave or other benefits to help cover the cost of time off due to illness or injury, these benefits may not be sufficient to cover all of your expenses.

You may not be able to rely on government benefits alone.

While government benefits such as state illness benefits may be available, they may not provide enough support to cover all of your expenses (could you live on €220 per week?).

How to Choose the Best Income Protection for Engineers

Alright, engineers, let’s talk about how to choose the right income replacement insurance policy.

This is the kind of decision you don’t want to take lightly – it’s like choosing your toppings, it can make or break your pizza.

So, let’s tuck into the factors you should consider when selecting a policy.

First up, occupation-specific coverage. As engineers, your job requirements and risks may differ from other professions, so it’s important to choose a policy that takes that into account. Look for policies that offer coverage tailored to your occupation, so you can have peace of mind knowing you’re protected against the specific risks you face.

Next, the deferred period. This is the length of time you have to be unable to work before your policy’s benefits kick in. It’s like waiting for a pizza to cook – seems to take forever, but it’s worth it in the end. Shorter waiting periods will cost more. Single applicants tend to go for 13 weeks, if your partner is also working, you should be fine with a 26-week waiting period. Consider your financial needs and risks when deciding on a waiting period that works for you.

The coverage amount is another important factor to consider. You want to make sure you have enough coverage to support your monthly expenses and maintain your lifestyle in the event of a disability. Think of it like choosing the size of pizza to order – you don’t want to order too big but definitely not too small, you want to find that sweet spot that’s just right.

Finally, inflation protection. This is like grating the parmesan on your pizza, you don’t really need it but it might just make your income protection *chef’s kiss helping ensure your benefits keep up with inflation over time. Look out though, some insurers are better than others for inflation protection so if you’re interested, please take advice from a broker who deals with all five providers.

Anyone hungry after all the pizza talk?

Now, onto the tips for selecting a policy that meets your specific needs and budget.

First off, shop around and compare policies from multiple insurers to find the best coverage and premium.

Also, consider the financial stability and reputation of the insurer. You don’t want to choose a policy from a fly-by-night company that could leave you in a lurch when you need it most.

FWIW, the companies we deal with – Aviva, Irish Life, New Ireland, Royal London and Zurich are financially sound although the larger established providers like Aviva have a proven history of paying claims fairly so that’s our recommendation (all other things being equal)

Finally, make sure you read the policy details carefully to understand the terms and conditions of coverage. Like the fine print on a contract – you want to make sure you know what you’re getting into. Hit me up if you want to see the specific T&Cs for a particular insurer.

In summary, choosing the right disability insurance policy is an important decision that requires careful consideration of several factors.

Keep these tips in mind when selecting a policy, and you’ll be well on your way to swiping right on the perfect financial partner.

How to Apply for Income Protection Insurance in Ireland

Now that you know why income protection insurance is so important, let’s talk about how to apply for a policy.

Applying for income protection insurance in Ireland is a straightforward process that typically involves filling out an application form and providing information about your occupation, income, health, and lifestyle.

It’s like filling out a job application, but for your finances.

To apply for income protection insurance, you’ll need to provide accurate and complete information on your application to ensure that your policy is valid and your benefits will be paid out if needed.

You may also need to undergo a medical exam or provide additional documentation to assess your risk level and determine your eligibility for coverage.

FAQs about Income Protection for Engineers in Ireland

Here are answers to some common questions that you may have about income protection insurance in Ireland:

What is the typical cost of income protection insurance in Ireland?

The cost of income protection insurance varies depending on several factors, including your age, occupation, health, and the level of coverage you choose.

Can I purchase income protection insurance if I have a pre-existing medical condition?

It may be possible to purchase income protection insurance with a pre-existing medical condition, but the terms and conditions of coverage may vary depending on the insurer and the condition. The insurer is likely to exclude the condition from your policy. So let’s say you suffer back pain, the insurer will exclude back pain from your policy so if you can’t work due to back pain, you won’t be abler to claim.

How do I file a claim if I become disabled and need to access my policy benefits?

To make a claim, you’ll need to complete a claim form and your GP will be asked for documentation of your disability to meet the terms and conditions of your policy.

Can’t get enough FAQs? Feel free to gorge yourself on our Income Protection FAQ Blog – How Does Income Protection Work?

What if I move abroad?

If you move to an EU country, your policy is still valid with most insurers – but double-check this before you sign up.

Over to you

In conclusion, income protection insurance is an essential consideration for engineers in Ireland who want to protect their income and financial well-being in the event of an unexpected setback. By understanding the application process, common questions, and tips for selecting a policy, you can ensure that you have the right coverage in place to keep you financially stable, even in difficult times.

If you have any questions or need assistance with selecting a policy, don’t hesitate to contact our brokerage for more information. We’re here to help you find the right income protection insurance policy for your specific needs and budget.

Ready to get started straight away – please complete this questionnaire and I’ll be back over email with some options and quotes.

Thanks for reading

Nick

lion.ie | Protection Broker of the Year 🏆

This blog was first published on 22/03/2023