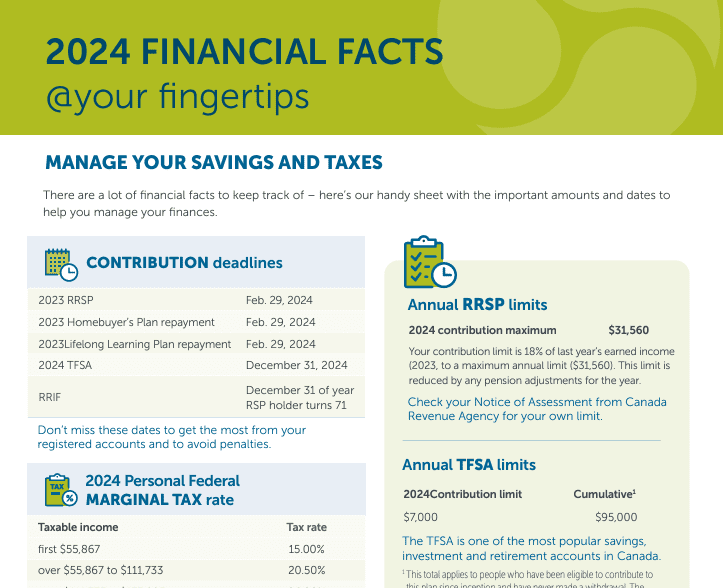

2024 Financial facts @ your fingertips

2024 FINANCIAL FACTS

@your fingertips

Manage your savings and taxes

There are a lot of financial facts to keep track of – here’s our handy sheet with the important amounts and dates to help you manage your finances.

![]() Download the PDF

Download the PDF

![]() Live in Quebec? Download the PDF

Live in Quebec? Download the PDF

CONTRIBUTION deadlines

CONTRIBUTION deadlines

2023 RRSP

Feb. 29, 2024

2023 Homebuyer’s Plan repayment

Feb. 29, 2024

2023 Lifelong Learning Plan repayment

Feb. 29, 2024

2024 TFSA

December 31, 2024

RRIF

December 31 of year RSP holder turns 71

Don’t miss these dates to get the most from your

registered accounts and to avoid penalties.

2024 Personal Federal

MARGINAL TAX rate

Taxable income

Tax rate

First $55,867

15.00%

over $55,867 to $111,733

20.50%

over $111,733 to $173,205

26.00%

over $173,205 to $246,752

29.32%

over $246,752

33.00%

Add your provincial marginal tax rates to get your

combined tax rate.

Lifetime capital gains exemption for qualifying small business corporation shares and farming and fishing property = $1,106,836

GROWTH in a tax-deferred plan

after 10 years*

Monthly deposit

3% rate of return

5% rate of return

$50

$6,987

$7,764

$100

$13,974

$15,528

$200

$27,948

$31,056

Register for a pre-authorized deposit plan for your

RRSP or TFSA and help your nest egg grow.

Annual RRSP Limits

2024 contribution maximum

$31,560

Your contribution limit is 18% of last year’s earned income (2023, to a maximum annual limit ($31,560). This limit is reduced by any pension adjustments for the year.

Check your Notice of Assessment from Canada Revenue Agency for your own limit.

Annual TFSA limits

2024 Contribution limit

Cumulative 1

$7,000

$95,000

The TFSA is the most popular savings, investment and retirement account in Canada.

1 This total applies to people who have been eligible to contribute to this plan since inception and have never made a withdrawal. The amount may be higher for individuals who made a withdrawal and wish to make a contribution in a year following the withdrawal.

LUMP-SUM PAYMENT

withholding taxes

All provinces except Quebec

Up to $5,000

10%

$5,001 – $15,000

20%

Over $15,000

30%

These taxes will be withheld at source from funds withdrawn from your RRSP, and from withdrawal amounts above your RRIF minimums. For non-residents of Canada, the withholding tax rate is 25%, but can be reduced by a tax treaty.

MANAGE YOUR RETIREMENT INCOME

CANADA PENSION PLAN (CPP)

monthly benefits

For January – December 2024

Average

Maximum

Retirement pension at age 65

$794

$1,365

Disability pension

$1,133

$1,607

Survivors’ benefit younger

than 65

$501

$739

Survivors’ benefit age 65+

$327

$819

Death benefit – one time payment

$2,498

$2,500

Yearly maximum pensionable earnings

(2024; 1st ceiling)

$68,500

Yearly maximum pensionable earnings

(2024; 2nd ceiling)

$73,200

CPP provides contributors and their families with partial replacement of earnings in the case of retirement, disability or death. You have to apply for the CPP retirement benefit — it doesn’t start automatically. If you get both a CPP survivor’s pension and a disability benefit, the total amount cannot be more then $1,614 in January 2024.

OLD AGE SECURITY (OAS)

monthly pension

For January-March 2024

Maximum

Pension at age 65

$713

Pension at age 75 and over

$785

Minimum Net Income Recovery threshold

(Income year 2024)

$90,997

OAS pension recovery tax

15% of excess

over threshold

It’s important to watch your annual net income, as the OAS recovery tax begins for net income over the threshold.

GUARANTEED INCOME SUPPLEMENT (GIS) monthly benefit

For January-March 2024

Maximum

Maximum if single, widowed, divorced, or if your spouse does not receive OAS pension

$1,066

Maximum if spouse receives OAS

pension or Allowance

$641

In addition to the OAS pension, low income Canadians may be eligible for GIS. Eligible seniors are automatically enrolled.

Talk to your advisor for more advice and information on managing your finances.

Age

RRIF/LIF

Minimum

Payment

60

3.33%

61

3.45%

62

3.57%

63

3.70%

64

3.85%

65

4.00%

66

4.17%

67

4.35%

68

4.55%

69

4.76%

70

5.00%

71

5.28%

72

5.40%

73

5.53%

74

5.67%

75

5.82%

76

5.98%

77

6.17%

78

6.36%

79

6.58%

80

6.82%

81

7.08%

82

7.38%

83

7.71%

84

8.08%

85

8.51%

86

8.99%

87

9.55%

88

10.21%

89

10.99%

90

11.92%

91

13.06%

92

14.49%

93

16.34%

94

18.79%

95 +

20.00%

This is the minimum you must withdraw every year from your RRIF/LIF (% of the market value).

* For illustration purposes only. Assumes monthly contributions made at the beginning of the period and compound annual returns.

Sources: Canada Revenue Agency, Government of Canada, Statistics Canada. This document is for information purposes only and is not meant to provide legal, financial, tax, or any other advice. Although care was taken in the preparation of this document, The Empire Life Insurance Company assumes no responsibility for any reliance on or misuse or omissions of the information contained in this document and cannot be held responsible for damages or losses arising from the use of this information. Please seek professional advice before making any decisions.

This blog reflects the views of the author as of the date stated. This information should not be considered a recommendation to buy or sell nor should it be relied upon as investment, tax or legal advice. Empire Life and its affiliates does not warrant or make any representations regarding the use or the results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use.

January 2024