Vitality Members Want To Share Data With Their Insurer

A behavioral change model successful in promoting healthier behaviors and successfully implemented in all the continents —

By Matteo Carbone, Founder & Director, IoT Insurance Observatory —

About 30 years ago, Adrian Gore and Barry Swartzberg harbored an intuition that introduced a different perspective on people’s well-being. This approach, known as Vitality, has since matured into a methodology primed to serve as a fundamental competency for any insurer in the future. The insurance sector has wholeheartedly embraced the notion of incorporating preventive measures, as aptly expounded in The Geneva Association’s publication titled “From Risk Transfer to Risk Prevention.” The imperative to cultivate less risky behaviors among policyholders in personal lines and among frontline employees in commercial domains stands as the indispensable path towards realizing this aspiration.

The conventional medical standpoint primarily centers upon employing medical interventions once a disease has manifested. In essence, this approach entails prolonging life by extending the period spent in somewhat suboptimal health, albeit with variations contingent upon the nature of the disease. Conversely, Vitality’s behavioral paradigm concentrates on promoting healthier lifestyle choices capable of elongating the duration of the policyholder’s time spent in a state of optimal well-being, thus further extending their lifespan.

A behavioral, proactive approach to healthcare (Source: Discovery)

Realizing these outcomes entails diminishing the frequency and severity of claims for the insurer. This incremental economic value is then partially channeled toward funding the expenses of the behavioral change program. At its core, the Vitality program involves – after adequately underwriting a risk – promising rewards to individuals exhibiting enhancements in their conduct. This, in turn, garners insurer’s enhanced technical outcomes from these shifts in lifestyle choices. A portion of these economic upsides is allocated to upholding these promises.

Over the past decade, this approach has been replicated in different markets – with different nuances program by program, and even one of the international partners has used Vitality as a stand-alone fee-based offer open to customers without any insurer policy – and has already attracted more than over 30 million[1] individuals globally. This journey has showcased an astonishing capacity to actively engage policyholders. Across numerous Vitality portfolios, a considerable majority of the members, exceeding two-thirds[2], have engaged in both physical and non-physical activities providing verified information. Nowadays, more than 100K new devices per month[3] are connected by members to the Vitality program.

Discovery has accomplished an enrollment rate ranging from 50% to 80% in their Vitality program among their South African policyholders. This remarkable achievement has been realized even with a monthly fee exceeding $17[4] charged to the insured for enrollment.

The international partnerships are yielding consistent evidence as well, demonstrating penetration rates of up to 70%[5] for Vitality in partners’ new business programs deployed in mature nations – even with a fee asked to policyholders to join the program and about five years on the market – and up to 80% in emerging economies[6]. Analogous outcomes have been replicated in corporate wellness initiatives, where as much as two-thirds of eligible employees have participated, in contrast to the industry’s average of 30% participation.

This engenders a virtuous cycle wherein policyholders crave to share their healthy behaviors with their insures and enjoy substantial advantages, with benefits that that the benefits can be higher than the premium paid. Simultaneously, this Shared-Value Insurance model allows the carrier to achieve superior results, thereby generating noteworthy positive externalities for society at large.

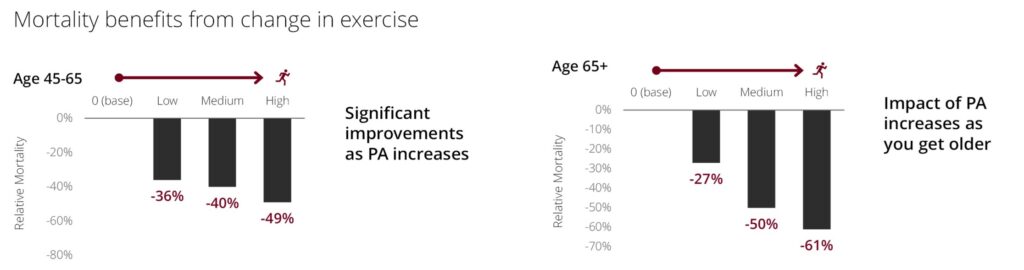

The foundation of the Vitality approach resides in promoting behaviors directly contributing to delaying diseases. Discovery’s three-decade journey provides robust evidence that a significant increase in the level of physical activity reduces by 49% the mortality for individuals aged 45 to 65, and a remarkable 61% reduction for those older.[7] Positive impacts have further manifested within annual medical expenditures, where the most engaged participants 15% lower claim cost[8] than the less engaged, risk-adjusted by age and medical conditions. A longitudinal study on the people who showed a low level of physical activity during the initial six-month period showed a subsequent 14% reduction in-hospital medical costs for the subgroup that notably elevated their engagement levels over the ensuing four and a half years.[9]

Mortality benefits from change in exercise (Source: Discovery)

As intuitively expected a program encouraging healthy behaviors and incentivizing individuals showcasing such conduct inherently possesses also the capability to attract and retain more people with a healthy lifestyle. In a demonstration of this effect, Discovery’s latest data pertaining to their SA health portfolio showed that the economic value the insurer garners through the Vitality approach is derived to the extent of 31% from the attraction and retention of younger members, and 20% from the attraction of individuals more likely to exercise. Consequently, nearly half of the accrued economic value can be attributed to behavior change—an elevated level surpassing the 28% recorded in 2016.[10]

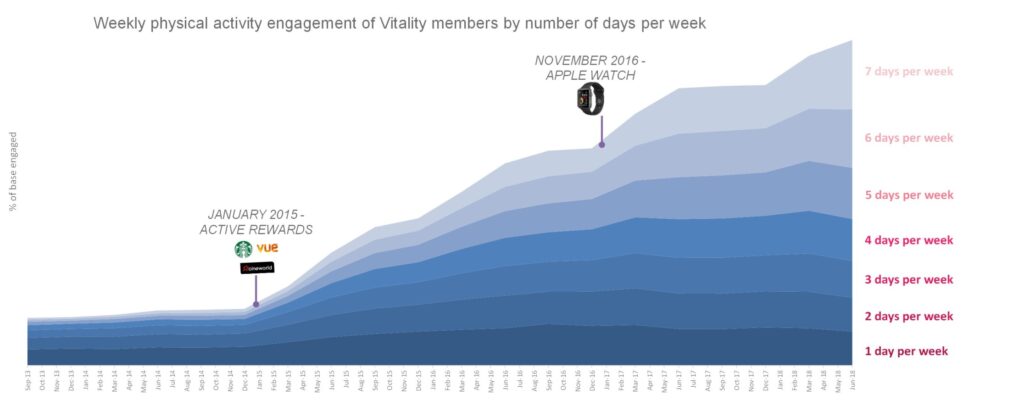

The enhancement evident in the attained outcomes is a direct outcome of Discovery’s continuous innovation effort. This ongoing endeavor has consistently honed their mastery in behavioral modification, seamlessly applying it across various geographical regions and lines of business. As illustrated by the figure below, the dynamic utilization of Active Rewards and loss aversion mechanisms (such as the mechanism to reimburse the Apple watch) – methodologies systematically tested and incrementally implemented across all programs over recent years – has showcased extraordinary efficacy in engaging members. This, in turn, has the direct causal effect of increasing the embrace of the desired healthy behaviors among Vitality’s members.[11]

Active Rewards and Apple Watch benefit impacts on the UK portfolios (Source: Discovery)

Upon examining the influence of Active Rewards on Discovery’s member physical activity, members who participated in Active Rewards saw more than a 20% increase in physical activity days regardless of their health status. This increase is observable across the entire spectrum of well-being, encompassing individuals categorized as “healthy,” “with stable chronic condition,” “with significant chronic condition,” and “with complex chronic condition.”[12]

An analysis of the physical activity patterns within the same member cohort, both prior to and subsequent to the implementation of these two advanced behavioral change methodologies, has yielded notable findings. Following exposure to Active Rewards, the average activity level exhibited a commendable upswing of 18%. Moreover, with the added incorporation of Apple Watch benefits, this average activity escalation escalated to an impressive 35%. This enhancement is consistently observed across diverse generational segments, with all age brackets showcasing increments surpassing 20%. Notably, individuals aged 50 and above displayed a particularly substantial uptick of 51%.[13] Similar pieces of evidence have been measured in South African, UK, US, and Australian portfolios.

The greater the proportion of engaged members, the higher the impact created on the insurer’s technical results. A Swiss Re’s “Health and Wellness Engagement Impacts” study examining a life insurance behavior change program estimated a threshold of 25% engagement as requisite to ensure a positive ROI for the insurer. Exceeding 90%[14] of Vitality’s markets with more than one year of maturity have already achieved engagement levels surpassing this specified threshold among members. One of the most effective international programs – a mature market – has reached a remarkable 64% engagement[15] rate among its members.

The provided evidence undeniably underscores the effectiveness of this approach—founded on technology and data shared by policyholders—in enhancing the Profitability of the insurance portfolio. This form of direct influence on technical results serves as a primary reason for the incorporation of any insurtech methodology within the insurance domain. However, when we embrace my 4Ps framework for evaluating insurtech initiatives an additional trio of impacts warrants consideration to focus innovation efforts within the insurance sector. These encompass Persistency, highlighting increased retention; Proximity, denoting frequency of interaction with the customer; and Productivity, indicating improved top line.

All Vitality portfolios have consistently demonstrated superior retention rates when contrasted with the broader market. Furthermore, the churn levels observed within the most engaged members typically range between one-third and half[16] of those observed in clusters exhibiting less healthy behaviors. This phenomenon exerts an exceptional influence upon the lifetime value of a policyholder cohort—what actuaries quantify as New Business Value—resulting in a shift in the quality of the insurance book.

The heightened level of engagement, described in the first part of the article – undoubtedly amplifies the frequency of interactions (app usage, push notifications, emails, …) between the insurance carrier and the policyholder. Several of the Vitality life portfolios have encountered an average above 20 touchpoints per month with policyholders[17], a marked departure from the traditionally minimal touchpoints associated with life portfolios. Noteworthy is a specific Vitality portfolio wherein the utilization of the insurer’s digital channels among members has surged more than fourfold[18] after the introduction of the above-mentioned Active Rewards.

One of Discovery’s international partners has disclosed the effect on cross-selling: the count of policies per customer is fivefold greater among Vitality members in comparison to the conventional portfolio.[19] An analogous trend is evident within an analysis of Discovery’s policyholder cohort with over five years of engagement. The examination reveals that the most engaged members maintain an average of 50%[20] more policies in contrast to their less engaged counterparts. This drive to increase productivity is the last but not least area of impact.

The sales performances are evidently influenced by a multitude of factors, encompassing the insurer’s strategy and initiatives, contingent market conditions, and competitive dynamics. Consequently, achieving an exact quantification of the impact of the Vitality approach proves to be a formidable challenge. Nevertheless, a plethora of anecdotal evidence lends credence to the notion that this facet could indeed be one of considerable significance:

A life portfolio growth fourfold the market, with market share rank from 11th to 7th in 4 years (mature country)[21];

Health carriers had a 33%[22] top-line growth over 6 years compared with a shrinking market (mature country);

A life bancassurance player increased market share from 2% to 7% in four years (emerging economy)[23].

This detailed overview demonstrates with facts and figures the effectiveness of the Vitality model – concretely achieving adoption and engagement among the entire spectrum of well-being – and the successful journey in replicating it in all the geographies.

Following the identification of the underlying causes of claims, this approach effectively incentivizes policyholders to disclose verified behavioral information, thereby securing rewards. This Shared-value mechanism serves to optimize their ongoing engagement while also yielding superior outcomes for the insurance enterprise, a portion of which is shared back to the policyholders.

Discovery has meticulously cultivated a suite of specialized competencies, encompassing the adept guidance of behavioral change, adept engagement with policyholders, the skillful orchestration of an ecosystem of retail partners to sustainably deliver appealing rewards, and a comprehensive array of supplementary aptitudes required to ensure the seamless integration and alignment of the Vitality approach across actuarial, marketing, and distribution functions. This prowess has been perpetually honed through collaboration with international partners and an unwavering commitment to continuous innovation.

Evidently, this methodology applied to health and life transcends the scope of a conventional wellness program, despite physical activity constituting a foundational incentivized component over its three-decade trajectory. It signifies an emergent insurance paradigm that holds the potential for extension across diverse insurance business lines (in South Africa, Discovery has successfully applied it to auto insurance). This extension aims to foster less risky behaviors among policyholders and, when deployed within commercial lines, extends its influence to encompass front-line employees.

Notes

1. Discovery website, https://www.discovery.co.za/corporate/investor-relations-about-us.

2. Discovery Group unaudited interim results for the six months ended 31 December 2022 (slide 9), https://www.discovery.co.za/assets/discoverycoza/corporate/investor-relations/2023/results-final.pdf.

3. Based on data from the Vitality Device Platform.

4. Discovery website, https://www.discovery.co.za/vitality/join-today/.

5. Discovery Group audited results for the year ended 30 June 2023 (slide 62), https://www.discovery.co.za/assets/discoverycoza/corporate/investor-relations/2023/results-final-fy-2023-update.pdf.

6. Discovery Group audited results for the year ended 30 June 2021 (slide 77), https://www.discovery.co.za/assets/discoverycoza/corporate/investor-relations/2021/fy-results-final-2021.pdf.

7. Discovery Group unaudited interim results for the six months ended 31 December 2022 (slide 21), https://www.discovery.co.za/assets/discoverycoza/corporate/investor-relations/2023/results-final.pdf.

8. Discovery Group unaudited interim results for the six months ended 31 December 2022 (slide 10), https://www.discovery.co.za/assets/discoverycoza/corporate/investor-relations/2023/results-final.pdf.

9. The case for getting active and driving well, white paper.

10. Analysis by Discovery Health Medical Scheme, 2020.

11. RAND Europe Study: Incentives and physical activity

12. The case for getting active and driving well, white paper.

13. AIA Vitality, Introduction to Active Benefits and Apple Watch Benefit, https://www.aia.com.au/content/dam/au/en/docs/press-releases/2022/apple-watch-insights.pdf.

14. Discovery Group unaudited interim results for the six months ended 31 December 2022 (slide 9), https://www.discovery.co.za/assets/discoverycoza/corporate/investor-relations/2023/results-final.pdf.

15. Discovery Group audited results for the year ended 30 June 2023 (slide 62), https://www.discovery.co.za/assets/discoverycoza/corporate/investor-relations/2023/results-final-fy-2023-update.pdf.

16. Sourced from data from various Vitality partners.

17. Why health and wellness initiatives matter for actuaries: John Hancock Vitality as a case study, John Hancock, 2019, https://www.soa.org/globalassets/assets/files/e-business/pd/events/2019/annual-meeting/pd-2019-10-annual-session-041.pdf.

18. Based on Discovery data.

19. Sourced from data from Vitality partner.

20. Based on Discovery data.

21. Sourced from data from Vitality partner.

22. Vitality partner market data compared with data from the 16th Edition of the LaingBuisson Health Cover report.

23. Sourced from data from Vitality partner.

About The Author

Matteo Carbone is the founder and director of the IoT Insurance Observatory, co-founder of Archimede Spac, and a global InsurTech thought leader and investor. He is internationally recognized as an insurance industry strategist with a specialization on innovation. Matteo is author and world-renowned authority on InsurTech – ranked among top international InsurTech Influencers – and he has spoken to audiences in twenty different countries. He published the first bestseller dedicated to InsurTech: “All the insurance players will be insurtech” and is member of the Forbes New York Business Council. Matteo has advised more than 100 different players in ten insurance markets around the world and has wide insurance experience which includes set up of industrial and commercial plans, growth strategy definition and support in the start-up of new initiatives, digital strategy development, insurance products innovation, channel strategy and commercial model definition, startups mentorship and advice M&A deals. He has worked directly with players accounting for more than 80% of the international IoT insurance volumes (number of policies on auto telematics, smart home, and connected health). Before creating the IoT Insurance Observatory and co-founding Archimede, he spent eleven years in Bain & Company’s Financial Service practice.

About IoT Insurance Observatory

The IoT Insurance Observatory is a global insurance think-tank which has put together executives from more than 70 insurance groups, institutions and the Internet of Things ecosystem to discuss the great potential of the most mature InsurTech trend, as well as the challenges it poses to the insurance business. The focus is on any insurance solution based on sensors for collecting data on the state of an insured risk and telematics for remote transmission and management of the data collected. For more information, visit iotinsobs.com.

SOURCE: Matteo Carbone