The Interpretation & Applicability (Or Inapplicability) of the Controlled Substance Exclusion of a Homeowners Policy (At Least in PA for the Time Being)

Although this decision is from the Pennsylvania Superior Court (intermediate appellate-level court), it’s interesting enough (at least to me and hopefully to you casualty coverage peeps) to copy and paste from my LinkedIn post of earlier today:

This decision befuddles me.

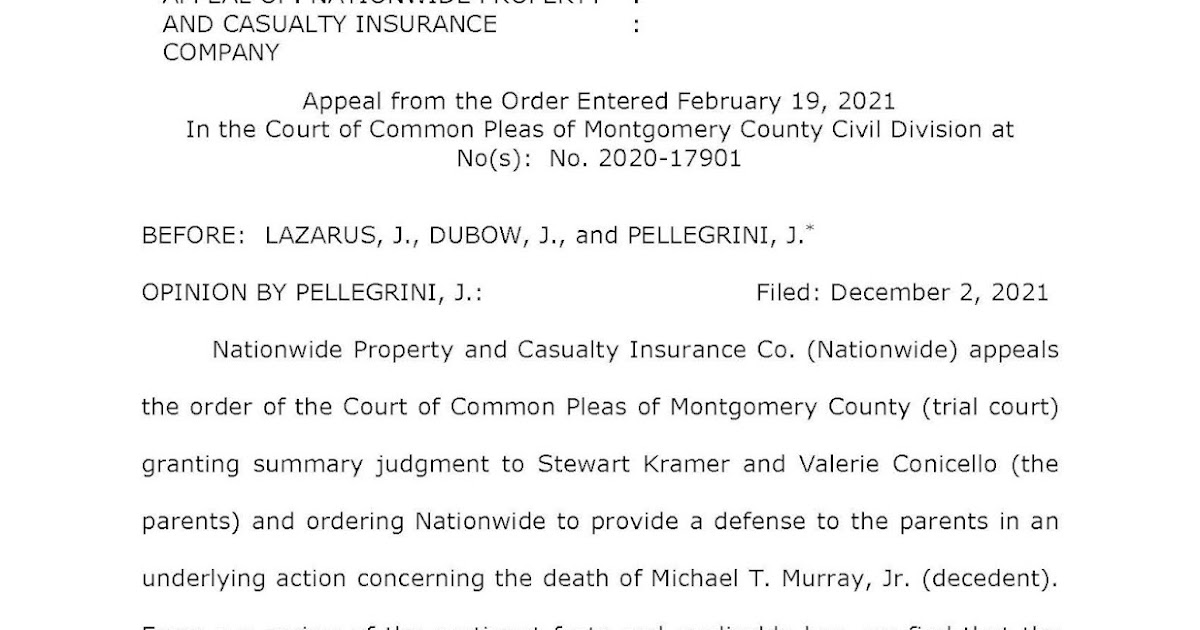

Nationwide insured the parents of Adam Kramer, who, while they were out of town, had Michael Murphy over to their home. Murphy later died of a drug overdose while at that home.

Murphy’s mother, Laurie Cruz, filed a wrongful death and survival action against Adam and his parents. Cruz alleged that at the time Adam hosted her son, Adam was widely known to use and sell controlled substances. Cruz asserted further that Adam was negligent in supplying the decedent with the drugs that caused his overdose. Relatedly, Cruz alleged in both the survival and wrongful death claims that the parents negligently allowed their son to use their home for such illicit activities.

The Nationwide HO policy pledged that Nationwide “will pay damages an insured is legally obligated to pay due to an occurrence resulting from negligent personal acts or negligence arising out of the ownership, maintenance or use of real or personal property.” (Bolding in original [meaning defined terms].)

The policy defined “occurrence” as “bodily injury or property damage resulting from an accident including continuous or repeated exposure to the same general condition.”

“Bodily injury” was defined as “bodily harm, including resulting care, sickness or disease, loss of services or death. Bodily injury does not include emotional distress, mental anguish, humiliation, mental distress or injury, or any similar injury unless the direct result of bodily harm.”

The policy excluded liability coverage, however, for “bodily injury or property damage … resulting from the use, sale, manufacture, delivery, transfer or possession by a person of a controlled substance[.]”

Based on that exclusion, Nationwide denied liability (defense and indemnification) coverage to the parents in the wrongful death/survival action. The policyholders sued and both parties moved for summary judgment.

In granting the parents’ MSJ, the trial court reasoned that the controlled substance exclusion did not apply because the parents’ alleged liability in the underlying action was rooted in negligence, which was distinct from the type of occurrence contemplated by the exclusion. [Huh?]

On Nationwide’s appeal a three-judge panel of the Pennsylvania Superior Court AFFIRMED the trial court’s order, finding that the policy’s controlled substance exclusion did NOT apply to negate coverage to the parents because:

…the wrongful death claim against the parents in the underlying action is not limited to bodily injury, as such damages are defined in the policy. The decedent’s family is also potentially seeking other types of damages rooted in its “emotional distress, mental distress or injury, or any similar injury,” none of which would be the direct result of bodily harm to the decedent’s family itself.

Since these are the types of damages that do not fall under the ambit of the policy’s “bodily injury” definition, the policy’s controlled substance exclusion would not apply to them.

Do you see the flaw in the court’s reasoning?

Here’s a hint: If the exclusion doesn’t apply because the decedent’s family’s claim against the parents doesn’t “fall under the ambit of the policy’s ‘bodily injury’ definition”, then…[finish this sentence].

Here’s another hint: What’s makes for a covered claim in the first instance?

Last hint (for those who ever attended any of my annual/biennial New York insurance coverage seminars): Is the light switch ON?

P.S. I think I figured it out.

Really last hint: The answer lies in how the court interpreted (and limited by enlargement) the policy’s BI definition. I’ve gone back and highlighted above some language from the court’s opinion. Get it now?