Second Home Insurance: Why It Costs More and How to Save

Introduction

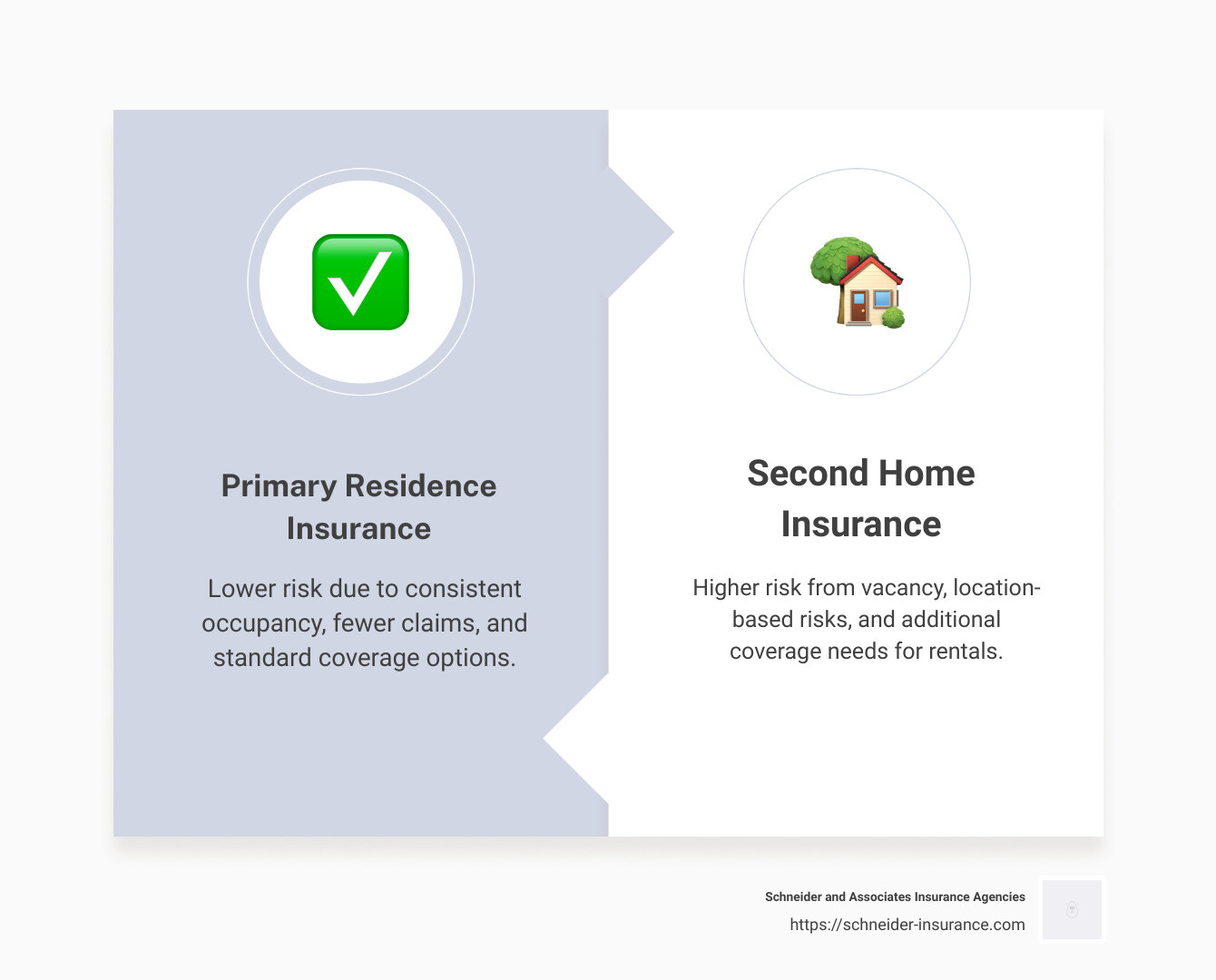

Is second home insurance more expensive? Yes, second home insurance is generally more expensive than insurance for your primary residence. Here’s a quick breakdown:

Increased Risk: Second homes are often vacant, leading to higher risks like burglary and unnoticed damage.Location: Properties in regions with severe weather, like wildfires or floods, cost more to insure.Usage: If rented out, the insurance needs to cover liability and potential tenant-caused damage.

If you own a second home, understand these factors. Second homes bring unique risks that your primary home may not face. Vacant periods, rental use, and even the type of location can all lead to higher insurance costs.

Our guide will help you understand why these insurance policies are more expensive and share practical tips to save on coverage.

Why Is Second Home Insurance More Expensive?

Risk Factors

Second homes come with unique risk factors that can make insurance more expensive. One major issue is that these homes are often uninhabited for long periods. When a house is vacant, it becomes more susceptible to risks like burglary, fire, and natural disasters. According to the Insurance Information Institute (III), a staggering 98.1% of homeowner claims in 2018 were due to property damage, including theft.

Imagine you own a cozy log cabin in the mountains. While it’s a perfect getaway, it’s also at higher risk for wildfires and snowstorms. These environmental risks can increase the coverage needed to insure your second home completely.

Another key factor is that vacant homes are more likely to have issues go unnoticed, such as water leaks or infestations. The longer these problems go undetected, the more damage they can cause, leading to higher insurance claims.

Specialized Coverage

Insuring a second home often requires specialized coverage. Unlike primary residences, second homes may need additional policies to cover specific risks. These policies typically include named perils, which specify exactly what is covered, like windstorms or fires.

For example, if your second home is in a flood-prone area, you may need a separate flood insurance policy. Flooding is a significant risk, and many standard policies do not cover it. According to Schneider and Associates Insurance, flooding can devastate your property, making separate flood insurance essential even if you’re not in a designated flood zone.

Another specialized coverage to consider is liability insurance. If you rent out your second home, whether short-term via platforms like Airbnb or longer-term, you’ll need coverage that protects you from potential tenant-caused damage. Landlord insurance can cover these risks and even help replace lost income if the property is being repaired.

In summary, is second home insurance more expensive? Absolutely, due to the unique risks and specialized coverage required. But understanding these factors can help you make informed decisions and find ways to save.

Next, we’ll discuss the key factors impacting second home insurance costs, including location, property type, and amenities.

Key Factors Impacting Second Home Insurance Costs

Location

Location plays a huge role in determining the cost of insuring a second home. Homes in flood-prone areas, like the swamp lands of Florida, or wildfire-prone regions, such as remote mountain cabins, are more expensive to insure. For example, a beach house in California may face storm surges and require additional hurricane coverage, driving up costs.

Property Type

The type of property you own also impacts insurance costs. Single-family homes often cost more to insure than condominiums or townhouses. This is because condos usually have a homeowners association (HOA) that provides some security and insures the exterior of the property. For instance, a condo in a ski resort area might be cheaper to insure than a standalone chalet.

Amenities

Amenities like pools, hot tubs, and security systems can affect your insurance premiums. Pools and hot tubs add risk, leading to higher premiums. On the other hand, installing security systems can lower your insurance costs by reducing the risk of theft and damage.

Age of Property

Older homes usually cost more to insure due to potential maintenance issues and outdated building materials. An old, neglected home will have higher premiums compared to a newer, well-maintained property. For example, an older beach house with outdated wiring and plumbing will be more costly to insure than a newly built, sturdy cabin.

Use of Property

How you use your second home also affects insurance costs. If you rent out your property, whether through Airbnb or as a long-term rental, you’ll need additional coverage. Landlord insurance can cover tenant-caused damage and even help replace lost income if the property is under repair. Vacation homes that are left vacant for long periods can be more susceptible to burglary and damage, increasing insurance costs.

Understanding these factors can help you make informed decisions and find ways to save on your second home insurance. Next, we’ll explore how to save on second home insurance costs through bundling policies, installing security systems, and more.

How to Save on Second Home Insurance

Bundling Policies

One of the easiest ways to save on second home insurance is by bundling it with your primary residence insurance. When you bundle policies with the same insurer, you often qualify for discounts. This can result in significant cost savings.

For example, if your primary home is already insured with Schneider and Associates Insurance Agencies, adding your second home to the same policy package could lower your premiums by up to 25%.

Installing Security Systems

Installing security systems is another effective strategy for reducing insurance costs. Alarm systems, smart home devices, and fire detectors not only protect your property but also make you eligible for discounts.

Smart home devices such as water leak sensors, smoke detectors, and motion sensors can mitigate risks and potentially lower your premiums. Insurers often offer discounts for homes equipped with these safety features.

Choosing a Low-Risk Location

The location of your second home plays a huge role in your insurance costs. Homes in areas less prone to natural disasters like floods, wildfires, or hurricanes are generally cheaper to insure.

For instance, a home further from the beach won’t be as susceptible to storm surges, which could lead to lower premiums. Similarly, choosing a property in a community with a lower crime rate can also help reduce costs.

Shopping Around

Finally, always shop around for the best insurance rates. Get quotes from at least three different insurers to ensure you’re getting the best deal.

Review your policy annually to see if you can find better rates elsewhere. Insurers like Schneider and Associates Insurance Agencies offer tools to help you compare quotes easily, so you can make an informed decision.

By following these tips—bundling policies, installing security systems, choosing a low-risk location, and shopping around—you can significantly reduce your second home insurance costs.

Frequently Asked Questions about Second Home Insurance

Is second home insurance more expensive than primary residence insurance?

Yes, second home insurance is typically more expensive than primary residence insurance. This is due to several factors:

Higher Risk: Second homes are often unoccupied for long periods, increasing the risk of burglary, vandalism, and unnoticed damage from events like fires or water leaks.Specialized Coverage: These homes may need additional coverage for risks specific to their location, such as flood or earthquake insurance.Location Risks: Vacation homes in desirable locations, like coastal or mountain areas, often face higher risks from natural disasters, which can drive up insurance costs.

Can I insure my second home under my primary homeowners policy?

No, you generally cannot insure your second home under your primary homeowners policy. Each home has unique characteristics and risks that require a separate policy. Your primary homeowners policy won’t extend coverage to a second home because:

Different Risks: Each property faces different risks based on its location, usage, and structure.Policy Requirements: Lenders and condo associations often require specific insurance for each property to protect their investment.

However, you may be able to bundle your primary and secondary home insurance policies with the same insurer, which can sometimes lead to discounts.

What additional coverage should I consider for my second home?

When insuring a second home, consider adding specific coverages tailored to its unique risks. Here are some key coverages to think about:

Flood Insurance: Essential for homes near water bodies or in flood-prone areas.Earthquake Insurance: Important for properties in seismic zones.Burglary and Theft Coverage: Useful for homes that are vacant for long periods.Liability Insurance: If you plan to rent out your home, this can protect you against claims from renters.Named Perils Coverage: This type of policy lists specific events (like fire, theft, or lightning) that are covered, which can be more cost-effective than a comprehensive policy.

Always consult with your insurance provider to tailor your coverage to the specific needs of your second home.

Conclusion

At Schneider and Associates Insurance Agencies, we understand that insuring a second home comes with unique challenges and risks. That’s why we offer personalized insurance solutions to ensure your vacation or rental property is fully protected.

Our team of experts will work with you to create tailored coverage that meets your specific needs. Whether your second home is a cozy cabin in the woods or a beachfront property, we have the right policy for you.

We pride ourselves on our local touch and deep understanding of the communities we serve. This allows us to provide you with the best advice and insurance options available.

If you’re ready to safeguard your second home, get in touch with us today. Let us help you rest easy knowing your investment is protected.