Pictures Explain Why There Is Coverage and State Farm Will Face Bad Faith at Trial

Pictures can speak a thousand words. In a coverage decision finding for the policyholder, those photos may speak hundreds of thousands of dollars.

The basic facts of the case were recited early by the court:1

Ms. Crigger owned 2,291 copies of a paperback book titled THE EARLY DAYS: AN INSIDE STORY OF NASHVILLE’S COUNTRY MUSIC BIZ; 4,500 posters of The Wendt Brothers; and 200 copies of the Pedal Steel.us magazine. All of those items were new and stored in the carport attached to her residence located at 745 Drummond Court, Nashville, Tennessee. Both the residence and carport were insured by State Farm.

The items were stored in a homemade container built by Ms. Crigger and Terry Wendt, who lived at the residence, but was not a named insured in the State Farm policy. Two sides of the container consisted of the outside rear walls of the main residence, while the other two sides were made of wooden privacy fencing. Plastic sheeting covered the top of the container to provide protection from the elements.

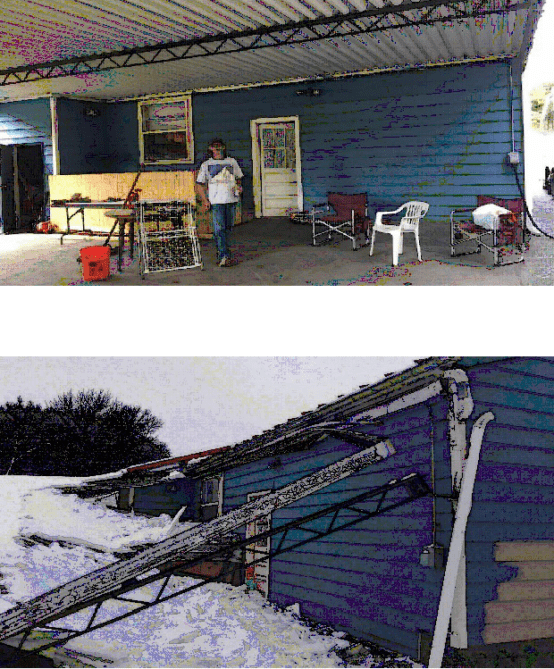

The court then placed before and after photos into the opinion:

Those photos obviously make one think—‘somebody is going to have coverage for the weight of snow causing a collapse.’ That is exactly what the court found, and that State Farm was wrong to argue that moisture damage was not covered:

Insofar as Ms. Crigger asserts that ‘the weight of the falling ice and snow caused the roof of the carport to collapse, and the ice and snow then fell onto the Personal Property that was inside a dry storage and melted,’ she presents a plausible claim for coverage under the ‘weight of the falling ice and snow’ peril. Likewise, State Farm presents a reasonable argument that there is no coverage because the weight of the falling ice and snow did not cause the damage, and water are not covered perils. And it is precisely because reasonable arguments can be made on both sides that State Farm is not entitled to summary judgment.

‘Tennessee law is clear that questions regarding the extent of insurance coverage present issues of law involving the interpretation of contractual language.’ Garrison v. Bickford, 377 S.W.3d 659, 663 (Tenn. 2012). Tennessee law is also clear that ‘contracts of insurance are strictly construed in favor of the insured, and if the disputed provision is susceptible to more than one plausible meaning, the meaning favorable to the insured controls.’

The reasonableness or plausibility of the competing arguments to the side, there are at least two other reasons why the Court finds coverage to exist under the policy. First, ‘the [policy] language in dispute should be examined in the context of the entire agreement.’ Phillips, 474 S.W.3d at 665. That examination suggests that if water damage and moisture were not a part of the peril encompassed by the ‘weight of ice, snow or sleet,’ then the policy would have made that clear – similar to the way that it made clear what was and was not covered in the event of a windstorm or hail:

2. Windstorm or hail. This peril does not include loss to property contained in a structure caused by rain, snow, sleet, sand, or dust. This limitation does not apply when the direct force of wind or hail damages the structure causing an opening in a roof or wall and the rain, snow, sleet, sand, or dust enters through this opening.

Second, the policy provides coverage for ‘accidental direct physical loss . . . caused by [a] peril.’ ‘Tennessee recognizes the concurrent cause doctrine, which provides that there is insurance coverage in a situation ‘where a nonexcluded cause is a substantial factor in producing the damage or injury, even though an excluded cause may have contributed in some form to the ultimate result and, standing alone, would have properly invoked the exclusion contained in the policy.’…Although State Farm argues that the concurrent causation doctrine ‘is inapplicable here’ because there was no ‘applicable peril that caused the loss,’ there is no dispute that the weight of snow and ice (a covered peril) caused the carport roof to collapse and the consequential melting of the snow and ice was a ‘substantial factor’ in the damage to Ms. Crigger’s personal property.

State Farm has certainly paid thousands of claims where personal property has been damaged by the snow and ice melting following a collapse. I guess the company was trying to find a new argument not to pay for those types of losses. The matter is set for trial early next year, and we will report on further developments if the case does not settle.

Thought For The Day

When I was young and ocean-racing competitively, and working the rest of the time, I was going 24 hours. I was on the verge of collapsing. But you’ve got to slow down a bit.

—Ted Turner

______________________________________________________

1 Crigger v. State Farm Fire & Cas. Co., No. 3:21-cv-00508 (M.D. Tenn. Sept. 6, 2022).