How popular modifications affect your car insurance

There’s a reason car manufacturers make cars the way they do: they want each model to appeal to the widest possible audience. But many car enthusiasts are keen to drive a car that’s modified to fit their particular set of preferences, whether those modifications be visual or performance-related.

The definition of a ‘modified’ vehicle, as far as insurance is concerned, is a vehicle that has been altered from factory standard (or since it has left the factory). This could be anything from installing a new engine to simply adding a bumper sticker, but every modification you make to your car comes with a compromise.

While some popular car modifications can reduce your insurance premiums, others increase them. Here, we take a look at some of the most popular car mods – along with their legality and their impact on your car insurance.

Jump to:

Popular modifications that may increase your insurance premium

Popular modifications that may reduce your insurance premium

Car mods that probably won’t affect your insurance

Do I have to tell my insurance company if I modify my car?

UK law specifies that if your car has been modified, you must declare the changes to your insurer, even if you didn’t make the changes yourself. If you don’t, your insurance could be invalidated.

As well as declaring any known modifications when you purchase your vehicle, it’s important to update your insurance company as and when you make additional changes to ensure you remain covered. Ideally, contact your insurer prior to making any modifications so that you can confirm any changes to your policy that may occur.

As the policyholder, the responsibility is on you to declare all modifications. If you’re buying a car second-hand and are in any doubt of work that may have been carried out, get the car checked by a mechanic.

What happens if I don’t declare modifications on my car insurance?

If you don’t declare the modifications – regardless of whether the omission was intentional – and you’re caught with undeclared mods, your claim may be refused and your insurance will be void.

If you have insurance refused or cancelled, you will find it harder and more expensive to get cover in the future. So, if you’re in any doubt, double-check and declare.

Depending on the modifications you plan to make, you may require a specialist policy, as not all insurers will cover modified vehicles. You may also find that a modified insurance policy will save you money, so it’s worth getting quotes, even if your current provider will cover you.

To find out more, read our blog, can insurers tell if your car is remapped?

Modifications that may increase your insurance premium

Engine upgrades

Modifications to your car’s engine and other vehicle mechanics, such as the exhaust system, transmission and air filter, can increase your vehicle’s performance. In 70-80% of cases where a car’s engine size is increased, insurance premiums increase too.

Engine Control Unit (ECU) remapping

The installation of an Engine Control Unit (ECU) is a good example of an engine modification that can push your insurance premiums up. All cars are set up at the point of manufacture to control the fuel-air mixture in the engine, which maximizes efficiency and power. Many manufacturers program the ECU’s parameters far below the car’s capability. Reprogramming, or ‘remapping’, this can improve engine performance and, in some instances, return better mileage.

Adding or replacing the ECU’s chip to make the car more economical will increase the brake force of the vehicle slightly. This may increase your premium, but only up to about 5%.

However, remapping the ECU to get substantially higher performance from your engine could cost more. As a general rule of thumb, the percentage increase to your premium will be about the same as the percentage increase in horsepower.

Cold air intake – filter modification

The installation of a cold air intake not only frees up the air flow to your engine, it also feeds it cooler, more condensed air. Cooler air is denser, bringing more oxygen into the combustion chamber and giving your engine more power as a result. This modification may only have a small impact on your premium, and won’t increase it as much as fully remapping your engine.

Exhaust upgrades

Many drivers relieve pressure on the engine – and return a little bump in horsepower – by improving the exhaust system, which aids waste flowing through the engine. This usually means making the exhaust bigger and louder, and may increase your premium.

Note that many ‘big bore’ exhausts are illegal, due to the amount of noise they make – usually because the exhaust silencers have been removed. UK law states that it is illegal to modify an exhaust system in a way that makes your vehicle noisier, and the police can take action if your silencer is missing or doesn’t work. If your exhaust system is illegal, you could face an on-the-spot fine and your car may be taken off the road until it’s returned to legal standards. And of course, illegal additions to your car will invalidate your insurance policy.

Upgraded brake discs

Carbon-ceramic discs and drilled or slotted discs (which allows for faster cooling as air passes through the holes) can be worth a lot of money. As such, installing them may actually increase your premium as a consequence of your increased car value.

Bodywork modifications

Body kits are often added onto existing bodywork, or replace current bodywork, resulting in the safety of the car being compromised. For example: adding a bigger bumper to make it look unique or sporty. While bumpers are made with safety in mind, body kits are not necessarily made to meet the safety standards required – sometimes crumbling under the tiniest of impacts.

Mods such as front and side skirts mean less ground clearance, which can be hazardous on uneven roads. Most body kits tend to be made of fibreglass or polyurethane, making them more likely to splinter in the event of a crash.

In general, if you have a standard policy, bodywork changes can increase your premium by 10-15%. However, if you already have a modified insurance policy, a body kit is unlikely to affect your premium unless it dramatically increases the value of your car.

The following cosmetic modifications can affect your car insurance in similar ways:

Flared wings

Wheel arches

Spoilers

Valances.

A popular body kit modification for Toyota MR2 owners is to transform their cars into Ferrari replicas. In cases such as these, the type of insurance policy you’re under may change. It’s always best to check with your insurance company before doing any work.

Gear short shift kits

Short shift kits are a popular modification that shorten the distance the lever needs to travel between gears. This means quicker shifts and sportier action – it can also make your car more difficult to drive if you’re not used to it!

As this modification is associated with young drivers and racing, it can be a concern for some insurers. That said, it will only increase your premium about 5-10% or maybe not at all if your car is already heavily modified.

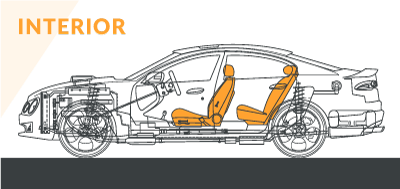

Custom interiors and exteriors

Reupholstering or replacing seats

Replacing or reupholstering your seats may be necessary depending on the age and wear of your car – or you might just decide you want to install heated seats or vintage-style tuck and rolls. Whatever the reason, make sure you mention the modification to your insurer.

Installing new seats or reupholstering your existing ones could increase a standard policy by 5-10%. If you already have a modified car insurance policy though, it’s highly unlikely new seats will incur any additional costs.

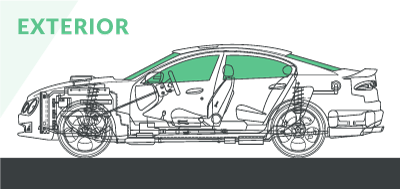

Custom paint jobs

Not all of the popular modifications you can make to your car’s exterior are legal. Exterior mods include, but are not limited to:

Tinted windows

Under-car neon lights

Custom LED headlights

Custom paint jobs

Stickers and decals

Adding a tow-bar.

Many people are surprised to hear that custom paint jobs, decals and stickers are also classed as a modification by insurance companies. As such, some people get caught out when they try to make a claim and discover their insurance isn’t valid because they haven’t declared their bumper sticker collection or racing stripes.

Not all insurance companies cover stickers and custom paint jobs – it depends on claims they have had in the past. If the company has had to make large pay-outs for cars with these kinds of modifications, they may not be keen to cover them for other drivers. For insurers that do offer cover, they’re only likely to increase your premium by 5% at most.

Alloy wheels

Alloy wheels are much stronger yet lighter than steel ones of the same size and can therefore improve car handling. This is because there will be less weight for the suspension to cope with and less resistance when you steer. Alloys are often ordered at the point of purchase for new cars, but they can also easily be an aftermarket modification.

If there’s a history of alloy wheel theft in the area where you live, your insurer may increase your premium.

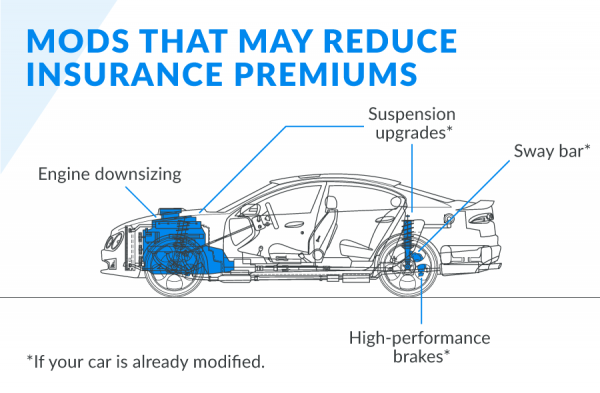

Modifications that may reduce your insurance premium

Engine downsizing

Many small engines are highly energy efficient, as they run on fewer cylinders and make the car lighter. For this reason, car manufacturers are opting for smaller engines in new cars. For existing cars, some people choose to swap their engine for a smaller one with the same power – getting the same performance but using less energy. Just as increasing engine size can increase your premium, downgrading to a smaller engine can decrease your premium.

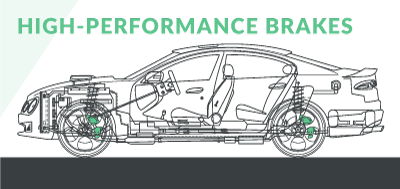

High-performance brakes

If your car has been fitted with uprated brakes, its behaviour on the road will be altered. Sports drivers, for example, will install high-temperature brake pads and fluid to get shorter, more consistent stops out of their brakes.

It is possible to install high-performance brakes into certain non-sports cars. If your car is already highly modified, an improved braking system may reduce your premium as much as 10-15%.

However, most cars are factory-fitted with suitable brakes already. If your car isn’t modified, or only has a few modifications like alloy wheels or suspension, your premium is unlikely to be affected.

Suspension upgrades

Upgrading your car’s suspension may make a noticeable difference to its handling, but most cars have adequate suspension as standard. As such, you’re unlikely to see a change in the cost of your policy, unless your car is already heavily modified – in which case, you may save about 5%.

Sway bars

When a car turns or swerves, the effect of the weight transfer onto one side can, over time, negatively impact handling. This is why some drivers install sway bars – also known as anti-roll or stabiliser bars – which help to reduce body roll by connecting the right and left wheels.

Rather than the car leaning to one side, the sway bar helps to distribute the force equally – the bar goes down on the side it leans into, and up on the other side. It’s a little extra that can save you about 5% if you have a highly modified car.

Car mods that probably won’t affect your insurance

While you must notify your insurance provider of any part of your car that is not factory standard, many modifications are unlikely to increase or decrease your insurance premium. We have some of these below.

Water cooling systems (brakes)

Another modification that improves brake performance is a water cooling system. For example, some cars have misting systems added to their brake ducts to keep them from overheating. These are unlikely to affect your insurance premiums.

Interior modifications

Sound systems

Sounds systems are a popular (and fairly cheap) mod. Most people will have seen – or more likely heard – a car with an aftermarket subwoofer. This is a speaker system designed to maximise low frequencies such as bass and sub-bass. Unless you opt for a high-value system, you won’t see a rise in your premium.

Dashboard add-ons and upgrades

You may modify your dashboard for functional reasons, such as adding a built-in satellite navigation system or car phone, or for aesthetics, such as switching to wood panelling. Either way, it’s unlikely to affect your premium.

Custom gear knobs

Gear knobs can also be modified. Some drivers will choose to replace their existing one because it is worn, or they’d prefer something more ergonomic or aesthetically pleasing (e.g. leather, sparkly). Novelty options include skulls, gaming joysticks and film prop replicas. They may affect your ability to change gear, but they probably won’t affect your insurance costs.

Exterior modifications

Novelty hub caps

Some car owners choose to make their mark on a car by customising their wheels, for example by adding spinning hub caps or light-up hub caps. While these can be a theft risk and you must notify your insurance provider, wheel modifications that are unrelated to performance are unlikely to affect your premium.

Do tinted windows affect insurance?

Tinted windows won’t increase or decrease your insurance cover, provided you ensure that they are legal.

While UK law states that there are no restrictions on tinting your rear windows and windscreen, the front windscreen and side-view windows do have restrictions. Legally, at least 75% of light must be allowed through the front windscreen and 70% of light through the front side windows.

That being said, you should still notify your insurer if you decide to tint your windows.

Is a tow bar classed as a modification?

Tow bars are classed as a modification because they differ from the manufacturer’s factory specification, so you should let your insurer know if you are fitting a tow bar to your car. That said, the addition of a tow bar is unlikely to increase or decrease your insurance premium.

Do wind deflectors affect insurance?

Wind deflectors are usually a manufacturer’s accessory and it’s unlikely that your insurer would raise your premiums as a result of fitting them. That said, they are a bodywork modification, so your insurer should still be notified if wind deflectors are being added.

Custom lights

Are headlight modifications legal?

Custom headlights are often illegal. By law, only white lights can be fitted at the front of your car, and red lights at the rear. Coloured LEDs are not allowed and could get you an on-the-spot fine, invalidate your insurance policy and leave your car off the road until it is declared road-legal again. This includes washer jet LEDs, which are prohibited.

What about under-car neon lights?

Under-car neon lights are a favoured modification. These can be fitted legally but by law, you are not allowed to have the tubing visible and the light cannot be so bright that it will distract you or other road users. For example, flashing under-car lights are illegal.

In general, lights won’t increase your cost of insurance. But your insurer may take into account your claims history and theft risk, especially if you’re a younger driver, and require a supplement.

Suspension modifications

Lowering your suspension

A car’s suspension can legally be lowered as long as this doesn’t affect the steering or headlight aim. There are strict specifications around headlight aim, as changes affecting headlights have the potential to dazzle other drivers.

Another issue faced with lowering a car is its ability to clear uneven road surfaces such as speed bumps. Over-lowering can also reduce the effectiveness of the car’s handling, putting the driver and passengers at risk. However, this modification is mainly cosmetic and unlikely to affect your premium.

Replacing bushings

Bushings are small rubber or polyurethane suspension components that are used to isolate vibration, provide cushioning and reduce friction between metal parts. Some drivers with rubber bushings replace them with polyurethane bushings, as these typically last longer and do a better job of quelling vibrations and minimising weight transfer.

These won’t affect your insurance policy, but as with all modifications, you should still declare them.

Racing elements

Track days became particularly popular in the 1990s after the introduction of speed cameras on Britain’s roads. As such, people started to modify their cars for the track by adding roll cages and roll bars. These are frames built into the car to protect the driver and/or passenger in the event of an accident.

It’s unlikely you’ll find an insurance company that will cover these under standard policies – you may need to consider a modified car insurance policy from a specialist insurer.

Other ways to reduce your modified car insurance premiums

Using security devices, such as immobilisers, tracking devices and additional safety locks, helps to discourage theft, and these are all ways to potentially reduce your premium.

If your car is a 1995 model or earlier, adding an immobiliser can eliminate your theft risk and therefore reduce your premium. Installing a tracker to a heavily modified car (£40,000 value or above) will also reduce the cost of cover for that vehicle.

Your premium is likely to be reduced by about 15% if you have bought a car and modified it yourself or had a mechanic modify it to your specifications. This is because the insurance company recognises that you have put time, energy and care into your car, and are less likely to treat it with disrespect or drive recklessly. In fact, some insurers will reduce your premium the more modifications you make!

Adrian Flux are specialists in modified car insurance. Why not get a quote by calling us on 0800 369 8590?