Why Paid-Up Additions Matter

Podcast: Play in new window | Download

If I had to pick one, and only one, additional feature of whole life insurance, it is hands down the paid-up additions feature. Even if I lose the ability to blend death benefit, if I still have the PUA feature, I’m in a position to augment policy value. This very special aspect of whole life insurance often goes overlooked and under-appreciated. Today I want to put it front and center of your attention. If you ignore my call to take notice, you do so at your own peril.

What Paid-up Additions can do for Whole Life Insurance

Paid-up additions are a versatile tool that can significantly augment policy values. Knowing about them, and how to use them, can unlock incredible performance in a whole life insurance policy. Paid-up additions can:

Substantially increase both policy cash value and death benefit

Create significant premium flexibility

Save your bacon when times get rough

Augment Cash Value and Death Benefit

Whole life insurance accumulates cash value over time as you pay the premiums. This accumulation of cash value is driven by two things. First is the guaranteed accumulation rate. This is the interest life insurers promise to pay you for paying premiums on your policy. Second is the dividend, this is a profit-sharing mechanism some life insurers share with their policyholders. You can squeeze out additional guaranteed interest and more dividends payable to you by attaching paid-up additions to your policy. Here’s a tabular synopsis of how much more money you can extract from whole life insurance through paid-up additions:

Year

No Paid-up Additions

Paid-up Additions

Difference

5

$ 27,177

$ 40,846

50.30%

10

$ 92,902

$ 109,792

18.18%

15

$ 179,754

$ 201,563

12.13%

20

$ 288,385

$ 320,510

11.14%

25

$ 430,021

$ 476,572

10.83%

30

$ 614,548

$ 680,287

10.70%

As you can see in the table above, you can achieve a huge increase in cash value from the outset of a policy. This big increase continues to benefit you with even more cash value well into the advanced age of the policy. Keep in mind that the total premium paid for both policies is identical.

Paid-up additions can also augment death benefit on a whole life insurance policy. Take a look at what simply using your dividend payment to attach paid-up additions to your policy can do for you:

Year

No Paid-up Additions

Paid-up Additions

Difference

5

$ 1,001,920

$ 1,025,945

2.40%

10

$ 1,004,500

$ 1,093,055

8.82%

15

$ 1,006,800

$ 1,195,698

18.76%

20

$ 1,008,920

$ 1,324,281

31.26%

25

$ 1,009,660

$ 1,456,100

44.22%

30

$ 1,010,790

$ 1,588,519

57.16%

From this table, we see that paid-up additions can create a substantially higher death benefit. Again the total premium paid is the same in both cases, but when we use paid-up additions, we create over a half-million-dollar increase in the death benefit 30 years down the road. For those worries about hedging inflation, this could be an excellent tool to accomplish this goal.

Premium Flexibility with Paid-up Additions

When you add paid-up additions to a whole life insurance policy through the paid-up additions rider, you now have a portion of premium that is discretionary. You don’t necessarily have to pay the rider premium for the PUA. So if a situation develops where you can’t or don’t want to pay the premium you originally planned, paid-up additions give you the flexibility of reducing your overall premium.

The chief concern we hear when discussing a whole life insurance purchase with someone is making a large commitment to pay a premium for years and years and years to come. Sure they have the money now. But will they have the money years from now? Paid-up additions can build lots of extra cash value AND reduce or eliminate some of the commitment fear.

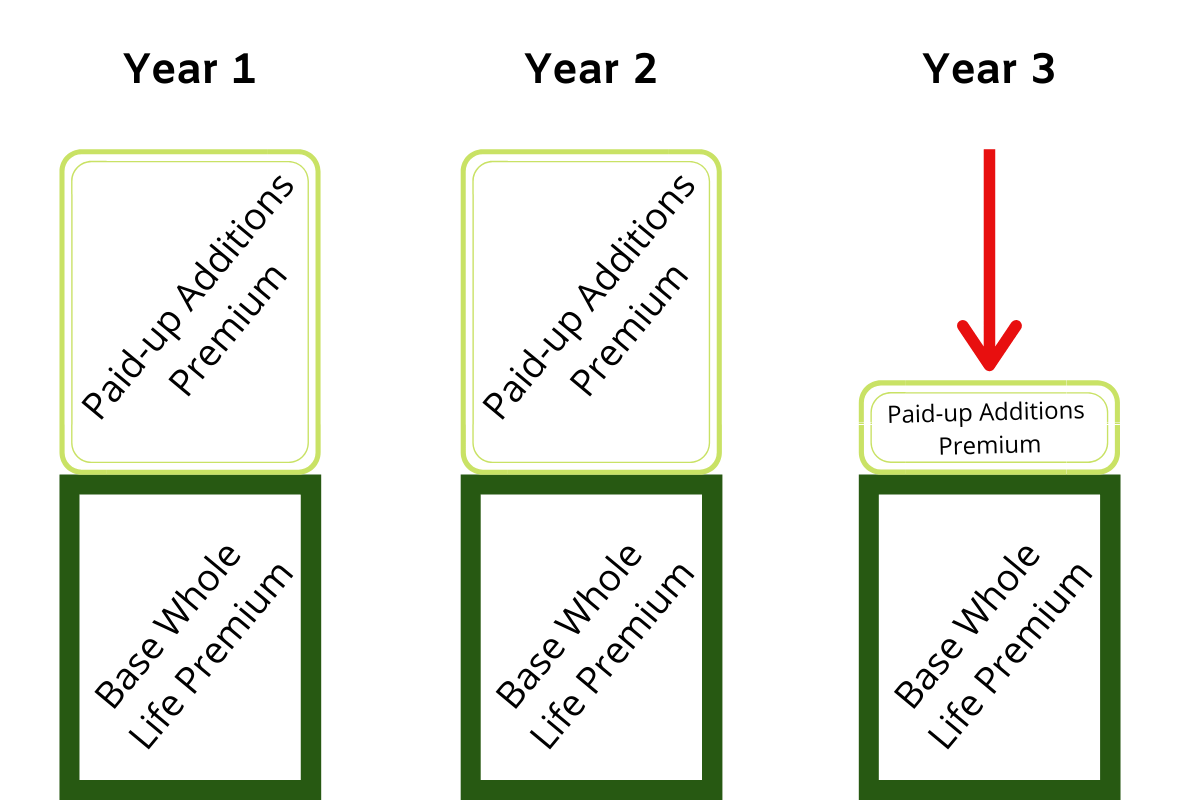

Here is a graphical example to further explain this idea:

From this example, we see that in year three the owner must make a reduction in the premium amount. He/she can easily accomplish this by making a reduction in the paid-up additions rider because this amount is always discretionary. Making this change to the premium will not risk policy lapse.

Paid-up Additions Protect you from Really Bad Times

Life is rarely a straight line. Instead it’s usually a continuum of twists and turns that leave many with an upset stomach more than once.

Paid-up additions can be a crucial lifesaver when life takes a trip into a valley. You can use accumulated paid-up additions in a number of ways to bridge a gap of uncertainty.

You can use paid-up additions to pay premiums due if cash flow is tight. This could reduce or completely cover your whole life premium. Provided you have enough paid-up additions accumulated, you can use them in this fashion for one or many years.

You can also take paid-up additions out of a policy by cashing them in and using them for whatever purpose you deem necessary. Life insurance isn’t hamstrung by the same accounting rules that impose penalties on accounts like IRA’s if you take money out prior to a certain age. You don’t have to qualify for a special circumstance to take the money out either. It’s your money and you can use it when you need it for whatever reason you want/need to use it.

Paid-up additions also count towards the cash value that you can borrow against through a traditional life insurance policy loan. So more accumulated paid-up additions enhance your ability to make use of the many fantastic benefits afforded by borrowing against your life insurance policy.

PUA: The Open Secret that Unlocks so much Value

With so many great features, you may find yourself asking “why doesn’t everyone talk about paid-up additions.” The sad truth is twofold.

On the one hand, paid-up additions offer very little compensation to sales managers so they have little incentive to spend much time training their agents to use the paid-up additions rider. This coupled with the fact that a larger whole life policy that incorporates paid-up additions might take a little while longer to close places a moderately strong disincentive to discuss it. Better to tell the newbies to focus on the little policies that close quickly so we all get paid before the end of the month!

On the other hand, it’s an advanced subject, so lesser experienced agents lack the skills and know-how to design and implement a policy using them. The notion that whole life insurance is a tool one can use for so much more than just death benefit protection trips up many. It’s little surprise, then, that novice insurance agents also struggle with the idea.

Despite this, paid-up additions are certainly available to just about anyone who purchases a dividend-paying whole life insurance policy. You’re well-advised to investigate further if your agent never mentioned them. If you are an agent, you’re well-advised to investigate further if your sales manager/up-line/etc. never mentioned them.