Largest Financial Firms Grapple With Worst Write-Offs in Three Years

The biggest U.S. banks are poised to write off more bad loans than they have since the early days of the pandemic as higher-for-longer interest rates and a potential economic downturn are putting borrowers in a bind.

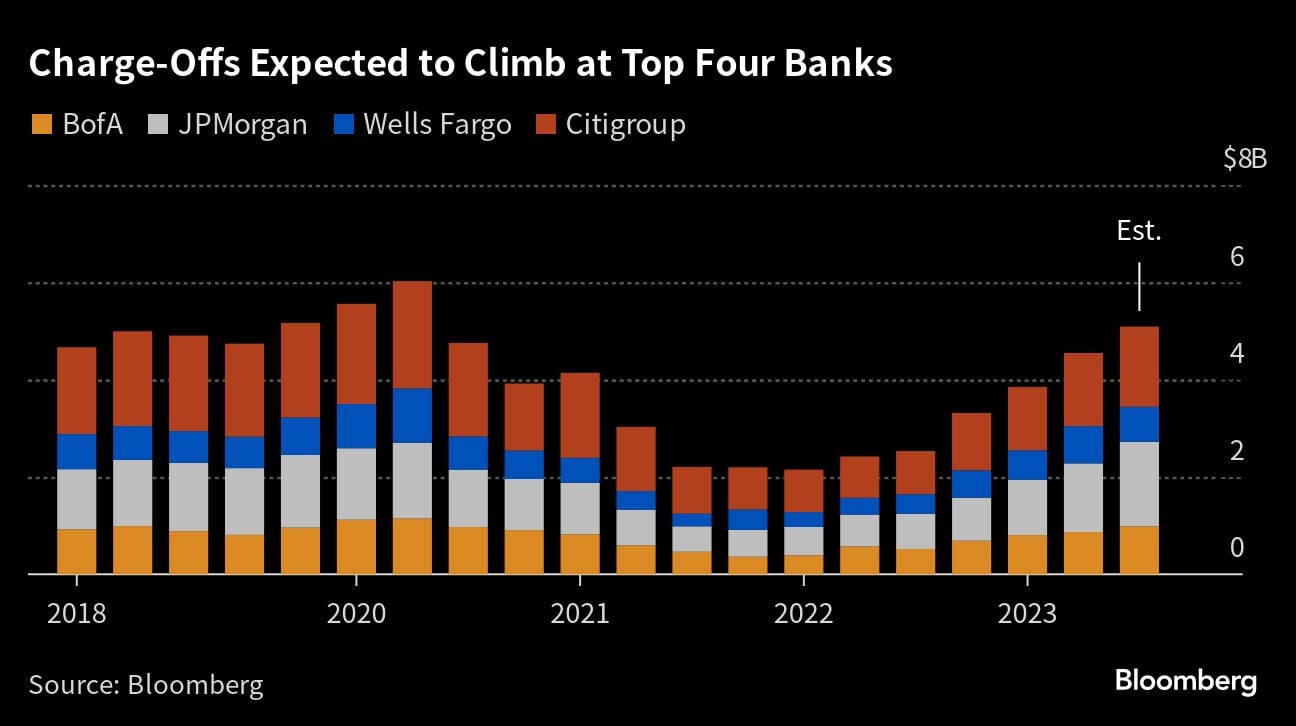

JPMorgan Chase & Co., Citigroup Inc. and Wells Fargo & Co., which report third-quarter results Friday, will join Bank of America Corp. — which comes Tuesday — in posting roughly $5.3 billion in combined third-quarter net charge-offs, the highest for the group since the second quarter of 2020, according to data compiled by Bloomberg.

The figure is more than twice as high as a year earlier, as lenders contend with consumers struggling to keep up with rising interest rates and a commercial real estate industry still grappling with fallout from the pandemic.

Citigroup Chief Executive Officer Jane Fraser said last month that her bank is starting to see signs of weakness in U.S. consumers with low credit scores, who have had their savings eaten away by historic levels of inflation. Still, she said the vast majority have been able to handle the rate increases.

“Any hiccups in credit will be punished by the market,” Erika Najarian, an analyst at UBS Group AG, said in a note to clients. “That said, there has been surprisingly little conversation about third quarter credit quality for large cap banks, even on either commercial real estate or some of the more publicized bankruptcies.”

Worsening credit quality suggests banks may have to set aside more money to cover sour loans should the economy deteriorate. Higher provisions to cover bad debt would eat into earnings.

Worsening credit quality suggests banks may have to set aside more money to cover sour loans should the economy deteriorate. Higher provisions to cover bad debt would eat into earnings.

In addition to deteriorating credit quality, analysts and investors will be watching prospects for net interest income — the difference between what banks earn on loans and how much they pay out on deposits. Looming increases in capital requirements and expectations for a decline in investment-banking revenue are additional headwinds.

Amid the obstacles crimping results, the KBW Bank Index has lost 23% this year, with Bank of America’s 18% drop the steepest among the four largest firms. New York-based JPMorgan is up 8.6% this year, the only one in the group showing a gain.

Here are some of the key metrics analysts will be watching:

Unrealized Losses

Banks’ securities portfolios will probably show an increase in unrealized losses in the third quarter after a steep rise in yields eroded the value of their investments, according to analysts. The Federal Deposit Insurance Corp. pegged second-quarter unrealized losses at $558.4 billion, up 8% from the period before.

But even if those losses increased, they don’t pose the kind of threat that ended up sinking Silicon Valley Bank, Signature Bank and First Republic Bank earlier this year. Deposits have stabilized since then, meaning lenders won’t be forced to sell the assets and book the losses.

Net Interest Income

NII probably dropped from the second quarter because of rising deposit costs and intensifying competition, trends that continued in the third quarter.

“Net interest income, which is a large source of revenue for the banks, will be under pressure in the near term as loan growth is subdued and deposit costs increase,” Jason Goldberg, an analyst at Barclays Capital, said in an interview.