The Life Insurance Shopping Path Is Too Quiet

What You Need to Know

The life insurance shopping process takes many consumers three or more months.

For a few weeks, consumers want to hear from you and insurers about life insurance.

Which consumers? And which weeks?

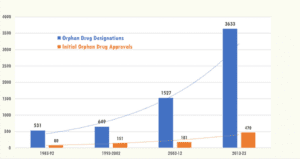

Life insurance demand fell precipitously between February 2021 and the end of 2022.

Activity levels have started to recover, a little, but, at Verisk, we saw 17 straight months of negative year-over-year growth in life insurance. The industry charted less application activity as a result.

http://images.thinkadvisor.com/contrib/content/uploads/sites/415/2023/04/2023-4-24-life-activity_Jornaya_800x460.png

Why did that drop in activity occur, and what can life insurance providers do to generate applications during slow periods?

Consumers have been facing sustained inflation and tightened budgets. The theory is that they are simply less interested in life insurance, and distracted by more immediate financial priorities.

Life insurance is a discretionary instrument; even in stable times, only 52% of Americans have any life insurance, and 106 million adults (about 41% of the U.S. adult population) do not believe they have adequate life insurance coverage.

Amidst the recent economic turbulence, even motivated life insurance shoppers have been letting existing policies lapse, or taking longer to buy new coverage.

You, the distributors and the insurers that write the coverage, have to work harder to reach new customers and retain current policyholders.

The Solution

Where there is risk, there is opportunity.

Savvy distributors are taking this time to build their capabilities, generate interest in a quiet market, and establish differentiated relationships with customers, powered by personalization.

While this may sound like a difficult strategy to implement, it’s more than feasible with the right tools.

Here are four steps to take to create demand in a down market.

1. Know who you want to sell to.

Not every consumer need is equal, and not every buying journey is the same.

Knowing the ideal customer for your offering is key to ensuring that your marketing efforts aren’t wasted on the wrong audience.

In today’s increasingly digital-first environment, it’s critical you leverage data to define your “ideal customer profile,” or ICP, keep your information on ideal customers complete and current, and be able to identify when you interact with an ICP shopper.

This starts earlier than you may think: 44% of life insurance applicants begin their shopping journey three or more months before applying.

When considering a life insurance policy, customers require time, conversations with their families and advisors, and a great deal of comparison shopping.

When a considerable amount of time is spent researching purchasing decisions, a shopper’s journey spans many websites, devices, and channels as well, so relying solely on your own first-party data is typically insufficient.

With first-party data, you may have a fragmented and outdated view of the customer’s entire shopping journey, making it difficult to create a personalized offer that will generate a differentiated conversation with a current life insurance shopper.

While insurance companies already own vast amounts of data, it’s often not well-structured, may be old or incomplete, and the logged interactions with the shopper are siloed within groups or divisions, with limited data sharing.

If this sounds familiar, working with a consultative data partner can help to better identify and segment your customer base and better understand how customers enter, engage with, and leave the business.

2. Find more people that look and act like your ideal customer.

Once the foundation is laid and you can accurately identify your ideal customer, it’s time to generate new shoppers.

Utilizing demographic details, personal attributes, and real-time shopping behavior will be crucial in maintaining the right audience for outbound marketing efforts.

Behavioral data completes the view of the customer by filling in their journey from beginning to end, including how they arrived at certain web pages and how they interact with your brand.

With the tools available to marketers today, it is fairly straightforward to identify every 35-year-old homeowner with a family, two cars, and an estimated household income of $75,000 or above.

Being able to scope your marketing campaigns to your ideal segments will create efficiencies in marketing and even down-funnel underwriting, enabling these functions to only focus on the most likely fits for your business.

And while these attributes are certainly important, layering on behavioral data can provide clues into the hearts and minds of the people you are trying to reach; this is the next level of life insurance marketing.

Gone are the days of spray-and-pray marketing strategies.

Now, marketers have the ability to send less ads and be targeted as to when to pop up in their ICP’s consideration set and what to say when they do interact with an ideal prospect.