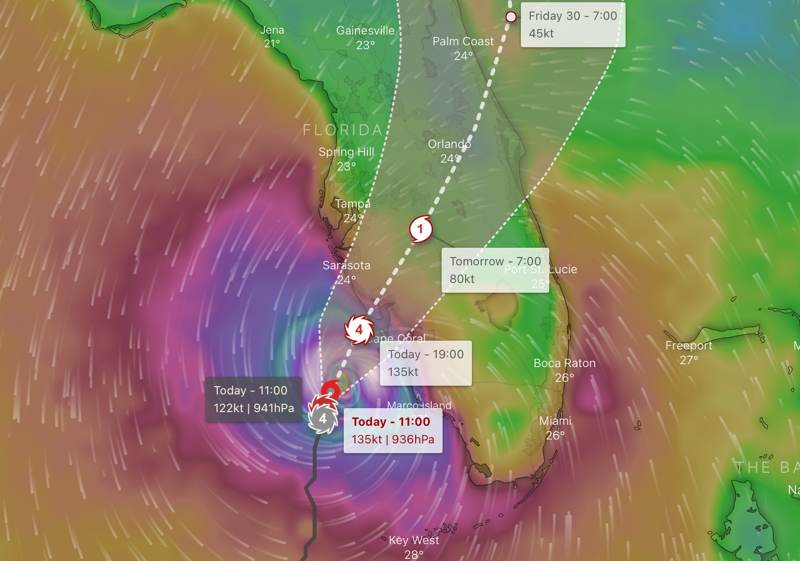

Cat modeller data hinted at hurricane Ian’s $50bn+ industry loss potential

According to sources, last night catastrophe risk modelling specialists had been hinting at major hurricane Ian having the potential to deliver a global insurance, reinsurance and ILS market loss of more than $50 billion, in updates sent to their clients.

We’re told these client updates featured modelled industry insured loss estimates for hurricane scenarios deemed to be most similar to hurricane Ian, so are provided as a service to help re/insurers and ILS fund managers understand the possible implications of a major catastrophe event.

As we understand it, these were wind and surge based industry insured loss estimates (with wind seen as the main focus) and provided to insurers, reinsurers, insurance-linked securities (ILS) funds and reinsurance managers, to help them understand the potential exposure to their portfolios, catastrophe bond and also collateralised reinsurance positions, with the numbers based on modelled estimations of events deemed similar to hurricane Ian.

As a result, these cannot be construed as attempts to issue precise modelled loss estimates based on hurricane Ian’s actual footprint and metrics.

As ever, official loss estimates from the main catastrophe modelling companies tend to take a few days or even weeks to become available, as is typical after any major catastrophe.

The reason for that being, it is still far too early for quality data on the real impacts of the storm to be available, so really the best that can be done soon after an event, or while it’s ongoing like last night, is a simulated storm-based estimate that is modelled across current exposure data, while true hurricane Ian footprint-based estimates will take some more days/weeks to be made available.

This information we’ve seen, which comes from some of the main cat modelling firms, is not that.

Rather it was based on catastrophe events from their respective database,s that are similar to Ian, in terms of size, strength and landfall location.

So, best guesses to help re/insurers, ILS fund managers and related reinsurance parties, to understand the potential impacts to their portfolios.

In fact, the industry loss estimate tends not to be the main driver of these updates to clients, rather it is the insights into how a storm could affect portfolios, specific cat bonds and reinsurance positions, that matters most. They provide further data to help portfolio managers understand their exposure as a result.

As we understand it, in these cat modeller updates from overnight, there was a reasonably significant leaning in the data towards a modelled estimate suggesting the industry loss could end up above $50 billion, with some scenarios pointing even higher than that.

However, as we’ve said before, there are similar scenario based modelled loss estimates that start lower down in the $20 billion’s, although it does seem the latest overnight data and our sources this morning now point more towards $30 billion becoming a lower-bound for the industry to work from, it seems (so perhaps $30bn to $50bn could be a new working range?).

These updates from cat risk modellers also highlight some catastrophe bonds that are felt to be at particular risk of loss, we’re told by sources, with the majority of those highlighted at this stage being Florida specific names, as well as some nationwide carrier sponsored cat bonds.

More broadly though, we’re told the data points towards a potentially significant erosion of deductibles for some aggregate and industry loss based cat bonds, but with them requiring additional events to occur during their risk periods, for any actual losses to be felt.

In the $50 billion ballpark, the industry loss from hurricane Ian would be close to a repeat of hurricane Katrina, so nearing the largest insurance and reinsurance market loss from a hurricane event ever and almost certaintly set to become the second biggest market loss from a hurricane in history.

At such a historic level of industry loss, the impact to insurance-linked securities (ILS) assets would be really significant, with losses set to fall across the asset class, from collateralized reinsurance through to catastrophe bonds.

Being modelled loss estimates, based on scenarios deemed similar to hurricane Ian, it is very hard to point to these figures as likely to prove accurate, of course.

But they do give a good sense of the scale of the re/insurance market impact that is anticipated with hurricane Ian.

It’s also worth noting, that these early and modelled scenario-based loss estimates, may not accurately reflect the current inflationary effects felt in the economy, or any loss amplification from assignment of benefits, litigation or social inflation related factors.

Uncertainty is going to remain extremely high in any estimates that come out today and over the coming days, as we said earlier today, this is a historic catastrophe for Florida, no matter the eventual quantum of industry losses.

Finally, it’s important to note the words “loss potential” in the headline of this article. It is just that, modelled estimates showing the potential for losses from similarly sized events, not an accurate representation of hurricane Ian’s costs and impacts to the industry. As said, that will begin to come over the days and weeks ahead.