Why Does Universal Life Insurance Have Such Low Guarantees

Podcast: Play in new window | Download

When looking at universal life insurance–especially in the context of its ability to accumulate cash value–and comparing it to other life insurance products like whole life insurance, people often note that it appears to have much lower guarantees. In fact, here’s an excerpt from an indexed universal life insurance proposal that highlights said low guarantee:Now, let me give you some background on this policy so that you can understand some of the amazement over this information.

This is an indexed universal life insurance policy for a male age 45. It has a death benefit amount of $815,241. If you’re wondering why the death benefit is such an odd number and not a neat round figure like $850,000 (for example), it’s because this policy was designed using the planned premium amount to calculate a necessary death benefit (I’ll elaborate a bit more on that in a bit). The planned premium for this policy is $50,000 annually (probably sounds extremely high if you’ve always thought of life insurance as an expense, but there’s something else we’re shooting for in this case).

Because this policy design uses a minimum Non-Modified Endowment Contract death benefit and is also complies with the Guideline Premium Test, that $50,000 premium is the maximum allowable without causing significantly unfavorable tax consequences to the policy.

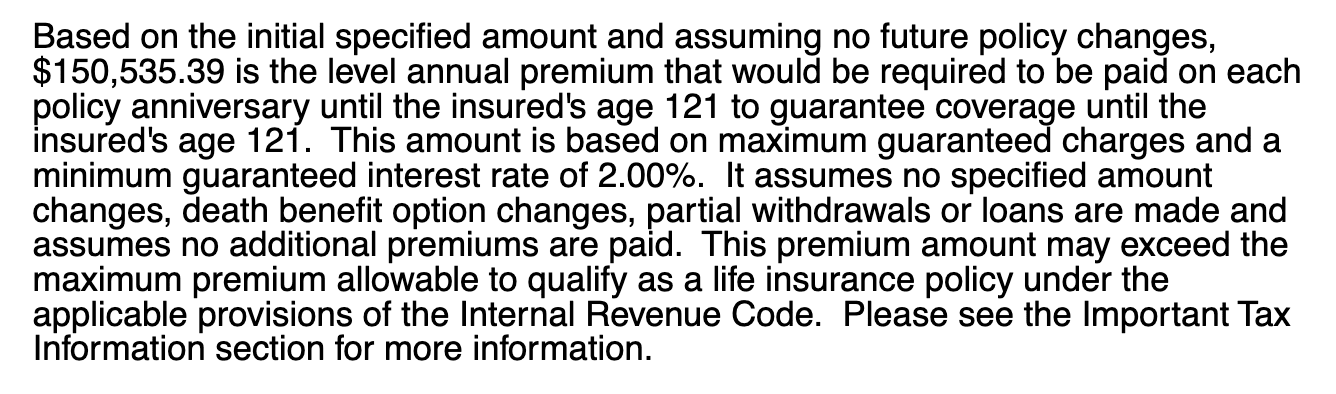

…but the quoted text, which was taken directly from the company-issued proposal, clearly states that if the would-be policy owner wishes to guarantee that his initial $815,241 death benefit remain in force to his 121st birthday, he much pay a whopping $150,535.39. This sounds terrible.

And if he really did desire to guarantee his death benefit to his 121st birthday, this would be an absolutely horrible product choice. But that’s not the goal here so this fact is…moot for the most part.

Different Life Insurance Policies Have Different Objectives

There are a lot of life insurance policies out there. And this may come as a surprise, but with all of this diversity of options comes a diversity of objectives tackled by different policies.

While many people understandably think of life insurance as universally the same–you pay a premium, and it pays a death benefit when you die–it is not. Some policies seek to offer a low-cost death benefit. Other policies seek to offer a high accumulation of cash value. Generally speaking, these two objectives are on opposing sides of a benefits spectrum.

If the individual in this situation wanted to guarantee an $815,241 death benefit to his age 121, there are products that would do it for far less than $50,000 per year-say nothing about the $150,535.39.

But if, on the other hand, he wants to achieve the highest rate of return on a $50,000 annual payment into a life insurance policy to build wealth that enjoys many tax benefits, this product is arguably the best currently available on the market.

Life Insurance Guarantees Cost Money

Life insurance guarantees cost money. This is true for both the insurance company and the policy owner. The insurance company must shoulder the risk associated with the death guarantee and have adequate reserves (i.e. money it holds but is very limited in investment options) to prove it can make good on the guarantee. This cost is most commonly realized to the policy owner through a lesser cash value accumulation on the policy.

Insurance companies are keenly aware of this tradeoff, and bring products to market that sacrifice guarantees in favor of providing much more attractive non-guaranteed features–usually expressed through cash value accumulation.

So in our example above, the product in question has such a low guarantee regarding the death benefit because it also has an extremely high potential to produce non-guaranteed cash value. The insurance company stripped high death benefit guarantees from the product in order to afford the ability to produce such higher cash accumulating features.

The same company offers other universal life insurance products. They have higher guarantees. They will almost definitely accumulate much lower amounts of cash value for the same premium as our 45-year-old male insured.